I recall discussing the situation and its financial implications with my then business partner as we commuted across the Golden Gate Bridge. More than two decades later, I have a strong sense of Deja-vu as we evaluate clients’ financial strategies in light of similar circumstances today.

As fixed income and muni market rates rise, the value of bonds go down. Municipal bond investors have a heightened awareness of the inverse relationship between interest rates and bond prices, but their knowledge of bonds, prices, yields and an extra dose of patience can be an advantage; they understand interest rates eventually will rise again.

For now, the Fed is planning to hold rates at near zero until labor markets reflect more maximized employment and inflation can reach 2% for some time. In this low interest rate environment, more bonds are being issued at premiums for sound reasons, and premium bonds can be used to help stabilize municipal bond values over time – if investors take time to understand them. When purchased correctly, premium bonds can work well in a portfolio and offer reasonable income solutions.

The Perks and Practice of Premium Bonds in Investment Portfolios

So, why would an investor want to pay a premium? Here are a few perks of premium bonds:

- They provide investors with a higher interest payment than par bonds or current market issues with small coupons, which allows cash to be returned at a faster rate.

- Those higher streams of cash flow annually can be reinvested for greater compounded returns, depending on where you invest it.

- In a rising rate environment, you have the advantage of investing systematically along with increasing rates at each semi-annual payment date.

- Higher coupon premium bonds have less sensitivity to rising interest rates than par priced bonds, also known as cushion bonds. The cushion is the difference between the higher coupon and market rates.

- Premium bonds can provide protection from a muni bond’s amount of exposure to downside values. They have less price volatility because market rates must catch up to bonds’ coupon rates.

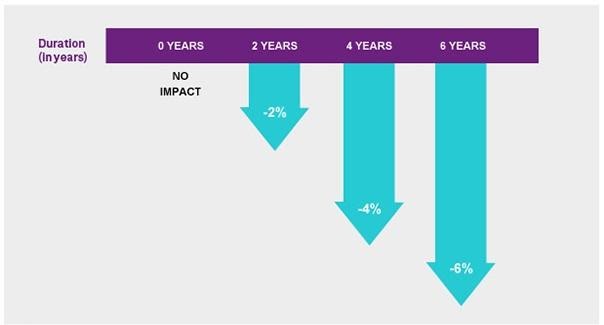

- In a period of rising interest rates, shorter bond durations are preferred, and higher coupons will shorten a bond’s duration. (Duration is the measure of the price sensitivity of a fixed-income investment to a change in interest rates.)

The Case for Concern in Using Premium Bonds

One of the biggest risks of premium tax-free and other bonds is if they are called early. This can result in a loss of principal to an investor. A quick rule of thumb is to look at the yield-to-call (YTC) on the bond and compare it to the rates of maturities available around your call date. It’s important to assess your risk compared to the potential reward of using premium bonds. In short, will the returns be more competitive than what a current market bond could provide?

Investors must factor in whether the bond is priced fairly and if the YTC or yield-to-maturity will provide a positive return when cashflows from the higher coupon rate are added. One must also consider the amortization of the premium paid above par (100) back down to par. The premium paid and amount received on the redemption of premium bonds are not deductible on tax-free bonds. Investors must amortize the premium, and according to the IRS this amortized amount is not a loss.

Change Is The Only Constant

Wayne Anderman CFP® MBA is the founder of Anderman Wealth Partners, based in the Greater Fort Lauderdale Area, and a registered representative of Avantax Investment ServicesSM. Member FINRA, SIPC. Investment advisory services offered through Avantax Advisory ServicesSM.

These opinions are based on Wayne Anderman’s observations and research and are not intended to predict or depict performance of any investment. These views are as of the close of business on 11/10/2020 and are subject to change based on subsequent developments. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. These views should not be construed as a recommendation to buy or sell any securities. Past performance does not guarantee future results.

Communications may not characterize income or investment returns as tax free or exempt from income tax when tax liability is merely postponed or deferred. Additionally, references to tax free or tax exempt income must indicate which income taxes apply or which do not, unless income is free from all applicable taxes. For example, if income from an investment company investing in municipal bonds is subject to state or local income taxes, this fact must be stated, or the illustration must otherwise make it clear that income is free only from federal income tax.