At first glance, today’s bond market appears relatively stable. Yields remain attractive compared to the ultra-low-rate era, corporate balance sheets have held up reasonably well, and economic growth has avoided a sharp downturn. For many investors, this combination has reinforced confidence in credit markets, particularly in corporate bonds.

But beneath the surface, a different reality is emerging. One of the most important signals in fixed-income—credit spreads—is flashing a warning.

While the broader environment may appear supportive, credit spreads have compressed to levels that leave little margin for error. This creates a paradox: investors are still reaching for yield, but they are being compensated less and less for the risks they are taking. In this environment, the traditional “buy the index” approach becomes more fragile, making selectivity, discipline, and active management critical tools for navigating risk and preserving returns.

Credit Spreads: Tight Levels and What They Signal

Bond investing is fundamentally about balancing risk with return. Because Treasuries are considered risk-free, investors venturing beyond them must measure the yield they receive relative to the risk they accept—and for that, they turn to credit spreads.

Credit spreads are the difference in yield between a corporate or riskier bond and a comparable risk-free government bond, such as a U.S. Treasury. They represent the extra compensation investors demand for taking on additional credit risk, including the possibility of default.

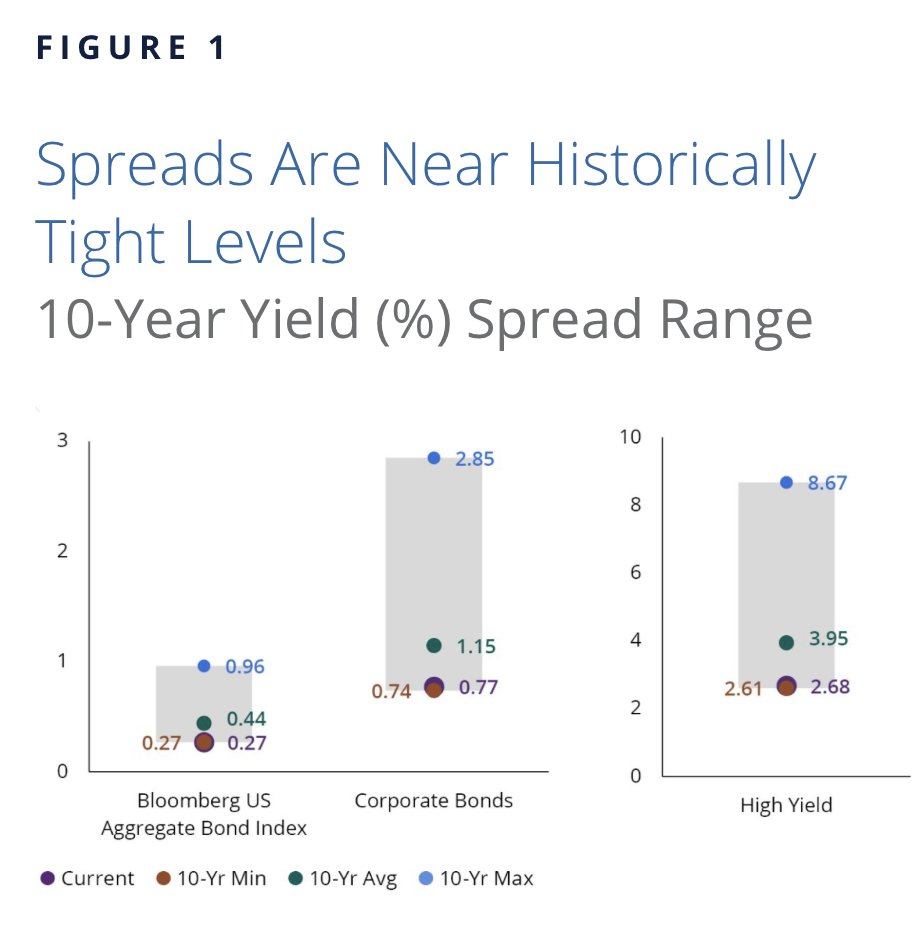

Right now, spreads are tight—perhaps too tight. They are near their lowest levels in almost 20 years. Investors tracking the Bloomberg Bond Aggregate Index are picking up only about 0.26 basis points over Treasuries, while investment-grade corporate bonds offer just 0.77 bps of extra yield. 1

This chart from Hartford highlights the historically tight spreads of the current bond market.

Source: Hartford Funds

Tight Spreads Increase Risk for Investors

At first glance, tight spreads may seem like a positive signal, suggesting investor comfort with credit risk and broadly healthy corporate fundamentals. However, this optimism comes with a cost: when spreads are narrow, investors are paid less for taking on additional risk.

The danger of tight spreads is not that they signal immediate trouble, but that they leave little cushion if conditions change.

Credit markets are influenced by both fundamentals and sentiment. As long as economic conditions remain stable and liquidity is strong, spreads can stay tight for extended periods. However, if sentiment shifts—due to geopolitical events, economic slowing, or financial stress—spreads can widen quickly.

When that happens, bond prices fall, and losses can accumulate rapidly.

This dynamic is particularly challenging because it often occurs after investors have already taken on additional risk in search of yield. In a low-spread environment, the temptation is to move into lower-quality bonds, longer maturities, or more complex structures to pick up incremental income.

But this “reach for yield” can backfire if spreads widen, leading to increased volatility and potential drawdowns.

Tight spreads also reduce diversification benefits. In calm markets, corporate bonds may behave similarly to Treasuries, but in periods of stress, they can act more like equities, declining as risk sentiment deteriorates. This combination can leave portfolios exposed to the least attractive features of both asset classes.

This is roughly the dynamic that played out in 2022/2023 when the Fed raised rates, as tight spreads exacerbated duration-induced losses.

Active Management in a Tight Spread Environment

Bond investors may have an edge in the current tight-spread environment, as active management tends to perform well in the asset class during these periods.

In a narrow-spread environment, simply owning the market or an index is no longer sufficient. The broad benchmark may offer limited return potential while exposing investors to asymmetric risks, making selectivity in where and how risk is taken essential.

Active managers bring several advantages to this challenge.

First, they can identify relative-value opportunities in the market. Even when spreads are tight overall, meaningful differences often exist across sectors, industries, and individual securities. Some bonds offer better compensation for risk than others, and active managers can exploit these discrepancies.

Second, active managers can adjust risk exposure dynamically. If spreads appear too tight, they can reduce exposure to lower-quality credit, increase allocations to higher-quality bonds, or shift across sectors, geographies, and maturities to manage risk more effectively.

Third, active management opens a broader opportunity set. Many of the most attractive fixed-income opportunities exist outside traditional benchmarks, including securitized assets, structured credit, and global bonds, where spreads may be more attractive and less correlated with traditional markets.

In short, active management helps investors navigate a market where the margin for error is thin—and right now, that margin is very thin by historical measures.

Active Bond ETFs

These ETFs were selected for their low-cost exposure to active bond management and are sorted by YTD total return, which ranges from 4.2% to 8.5%. Expenses range from 0.15% to 0.70%, assets from $409M to $14B, and current yields from 4.2% to 7.3%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| BOND | PIMCO Active Bond ETF | $5.9B | 8.5% | 5.1% | 0.71% | ETF | Yes |

| JCPB | JPMorgan Core Plus Bond ETF | $8B | 8.2% | 5.06% | 0.40% | ETF | Yes |

| AVIG | Avantis Core fixed-income ETF | $1.3B | 7.8% | 4.5% | 0.15% | ETF | Yes |

| VPLS | Vanguard Core Plus Bond ETF | $841M | 7.7% | 4.2% | 0.2% | ETF | Yes |

| TOTL | SPDR DoubleLine Total Return Tactical ETF | $3.9B | 7.5% | 4.9% | 0.55% | ETF | Yes |

| FLHY | Franklin High Yield Corporate ETF | $635M | 7.3% | 6.2% | 0.40% | ETF | Yes |

| BINC | BlackRock Flexible Income ETF | $13B | 6.5% | 4.9% | 0.52% | ETF | Yes |

| HYDB | iShares High Yield Systematic Bond ETF | $1.7B | 6.5% | 7.1% | 0.35% | ETF | No |

| HYBL | SPDR Blackstone High Income ETF | $511M | 5.8% | 7.2% | 0.70% | ETF | Yes |

| YLD | Principal Active High Yield ETF | $409M | 5.7% | 6.8% | 0.39% | ETF | Yes |

| JPST | JPMorgan Ultra Short Income ETF | $34B | 4.6% | 4.4% | 0.18% | ETF | Yes |

| SRLN | SPDR Blackstone Senior Loan ETF | $6.9B | 4.6% | 7.3% | 0.70% | ETF | Yes |

| MINT | PIMCO Enhanced Short Maturity Active ETF | $14B | 4.2% | 4.5% | 0.35% | ETF | Yes |

The bond market is offering attractive yields, but the underlying risk dynamics are more complex than they appear.

With credit spreads near historic lows, investors are being paid less to take on risk at a time when uncertainty can resurface quickly, creating an environment where the margin for error is thin and passive approaches may struggle to deliver optimal outcomes.

Active management provides a way forward. By emphasizing selectivity, flexibility, and disciplined risk management, active strategies can help investors navigate tight spreads and position portfolios for both income and resilience.

Bottom Line

With credit spreads near historically tight levels, investors are being paid less to take on risk just as uncertainty can quickly resurface, leaving portfolios vulnerable if conditions shift. This makes broad, passive credit exposure less compelling and reinforces the case for active management.

1 Hartford (March 2026). When Credit Spreads Leave Little Room for Error