The fixed-income landscape has undergone a notable transformation. With the end of the ultra-low interest rate era, bonds now present compelling yield and income prospects. At the same time, heightened rate volatility, persistent inflationary pressures, and evolving credit conditions have introduced a more complex environment marked by both challenges and opportunities.

Despite these changes, many investors still rely on the Bloomberg U.S. Aggregate Bond Index— better known as the “Agg” — as the foundation of their bond portfolios. For decades, the Agg has been viewed as the default benchmark for core fixed-income, a broad representation of the U.S. investment-grade bond market.

The reality today is that the Agg no longer reflects the full opportunity set available to investors. Increasingly, investors are turning to multi-sector and core-plus fixed-income strategies as a more modern approach—one that better aligns with today’s dynamic bond market.

The Agg Falls Short

The Agg was designed in a different era, when the fixed-income market was simpler and more constrained. Government and investment-grade corporate bonds were virtually the only options available, and the index provided a genuine benchmark for the bulk of the fixed-income market.

While it still serves as a useful reference point, its limitations have become increasingly apparent.

The Agg features significant concentration in U.S. Treasuries and agency mortgage-backed securities. These assets provide stability but tend to offer lower yields than other areas of the bond market, meaning investors relying on the Agg may earn less income than a more diversified approach would deliver.

The Agg is also constructed based on the amount of debt issued rather than investment attractiveness, so the largest borrowers—primarily the federal government—receive the largest weights regardless of whether they offer compelling value. In essence, the Agg allocates capital based on supply rather than opportunity, which can lead to suboptimal outcomes when other sectors offer better risk-adjusted returns.

These limitations have hurt the index and passive investors in recent years, with the Agg underperforming many fixed-income market segments since roughly the Great Recession.

Multi-Sector Credit Is a Better Approach

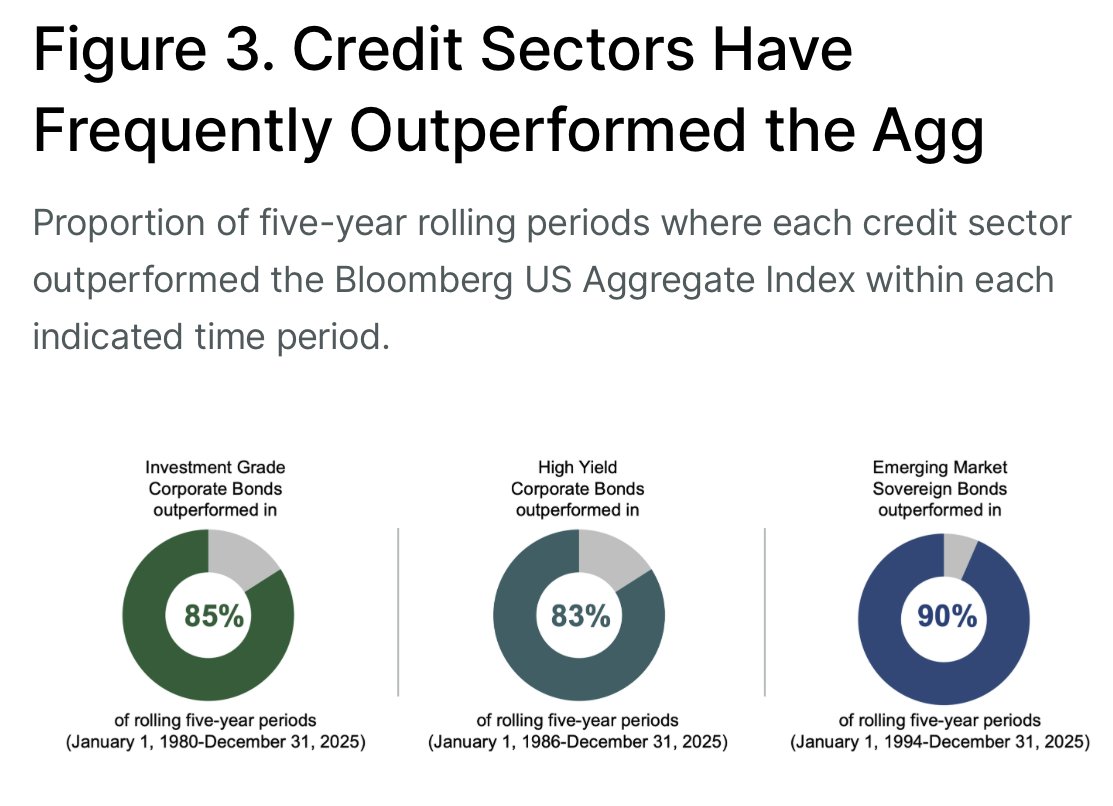

This underperformance is visible in the data. Looking at five-year rolling periods across various credit sectors versus the Bloomberg U.S. Aggregate Index, Lord Abbett shows that most credit sectors outperform the Agg the majority of the time. The chart below from the asset manager highlights that outperformance over time.

Source: Lord Abbett

According to Lord Abbett, the mixed performance of the Agg versus other credit sectors underscores an idea investors often overlook: the role of credit in portfolio allocations isn’t just about diversification or dampening equity volatility—it should also be about generating income and attractive returns.

This is why it may be time to move beyond the Agg for bond exposure. Multi-sector credit strategies offer a more flexible and comprehensive approach to fixed-income investing, spanning investment-grade corporates, high-yield bonds, emerging market debt, securitized assets, loans, and other credit instruments.

This broader opportunity set allows investors to capture income and returns from multiple sources rather than a narrow market segment. Instead of starting with a narrow benchmark and adding satellite exposures, investors can build portfolios that are inherently diversified and opportunity-driven—an approach that aligns more closely with today’s complex, interconnected markets.

The data support this shift. According to a recent Fidelity Institutional study, the Agg has not outperformed the average multi-sector portfolio on returns in a single year over the past decade.

Dumping The Agg For Good

By combining different sectors and actively managing allocations, investors can potentially enhance returns while mitigating risks. This ability to generate alpha is a key reason why multi-sector strategies have grown significantly in recent years.

It may finally be time to replace the Agg with multi-sector credit as core bond exposure. For investors ready to make that move, active ETFs offer one of the most practical implementation options, allowing flexible, active strategies to be incorporated directly into a portfolio.

Multisector Active Bond ETFs

These ETFs provide low-cost exposure to active bond management across unconstrained, dynamic, go-anywhere sectors. Sorted by YTD return—from 7.6% to 9.1%—they carry expense ratios between 0.10% and 0.56%, assets between $51M and $22B, and current yields between 4.2% and 6.8%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| BOND | PIMCO Active Bond ETF | $6.6B | 9.1% | 5.0% | 0.56% | ETF | Yes |

| JCPB | JPMorgan Core Plus Bond ETF | $8.8B | 8.7% | 5.30% | 0.40% | ETF | Yes |

| OBND | SPDR Loomis Sayles Opportunistic Bond ETF | $51M | 8.10% | 6.8% | 0.55% | ETF | Yes |

| FBND | Fidelity Total Bond ETF | $22B | 7.9% | 4.9% | 0.36% | ETF | Yes |

| VCRB | Vanguard Core Bond ETF | $3B | 7.85% | 4.20% | 0.10% | ETF | Yes |

| TOTL | SPDR DoubleLine Total Return Tactical ETF | $4B | 7.84% | 5.1% | 0.55% | ETF | Yes |

| DBND | DoubleLine Opportunistic Bond ETF | $600M | 7.6% | 5% | 0.45% | ETF | Yes |

| BINC | BlackRock Flexible Income ETF | $14B | 7.59% | 5.5% | 0.52% | ETF | Yes |

The Agg has served investors well for decades, but the fixed-income landscape has changed.

Today’s bond market is broader, more complex, and full of opportunities beyond traditional benchmarks. Relying solely on the Agg may limit investors’ income, diversification, and return potential.

Multi-sector credit offers a compelling alternative. Its flexibility, broader opportunity set, and ability to adapt to changing market conditions make it a more modern and effective approach to fixed-income investing.

Bottom Line

In a world where opportunity is no longer confined to a single index, the message is clear: it may be time to move beyond the Agg and embrace a more dynamic approach to bonds.

1 Lord Abbett (February 2026). The Case for Multi-Sector Credit