In theory, bond yields should decrease. As inflationary pressures appear to be fading and data indicate declines, the Federal Reserve has started to cut rates. However, conventional wisdom and widespread assumptions do not always play out, and bond yields are actually rising.

And those yields could reach unprecedented highs.

The calls for 6% yields on Treasury bonds are increasing, leading to various allocation decisions. The path to 6% may be volatile and bumpy, but the returns should be excellent once attained.

Three Main Factors

While it may have been unthinkable in the years following the Great Recession and during the pandemic, the road to 6% Treasury yields is now possible, according to T. Rowe Price and other fixed-income experts.

Bond yields have already risen as the Fed combats the post-pandemic inflation. The jump in interest rates led to a decrease in bond prices and an increase in yields. New bonds entered the market where bonds are yielding more. This inverse relationship has been standard for the bond market—particularly Treasury bonds—for quite some time. The reverse also holds: as the Fed cuts the interest rate, bond yields should fall to reflect the change.

However, right now, as the central bank cuts rates, bond yields continue to climb. The reasons for the higher yields, despite the rate cuts, are threefold.

For starters, fiscal concerns are influencing fixed income. The recently enacted “One Big Beautiful Bill” is set to keep the U.S. deficit high for the foreseeable future, with projections estimating the bill will expand the deficit by about $3 trillion to $4 trillion over the next decade. This will push the ratio of debt to gross domestic product (GDP) to new highs.

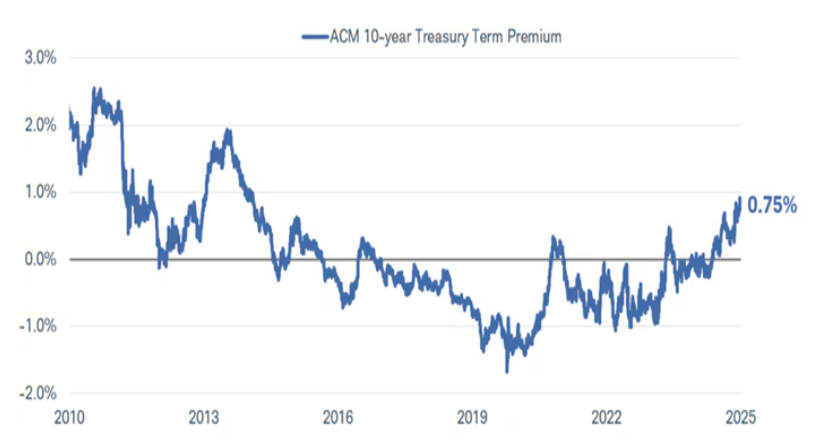

For many investors, this puts the U.S. in a precarious position, and they now demand more yield to hold longer-term debt. This extra yield is the term premium. Since the Liberation Day tariff announcements, the term premium on the benchmark 10-year is now at its highest level in more than a decade. This chart from Charles Schwab highlights the recent uptick despite lower rates.

Source: Charles Schwab

In addition to the higher yield due to higher term premiums, the Fed may not be able to cut rates too low because expansionary growth and inflation are approaching.

While the tariffs have limited growth potential across the world, many nations and regions—including China, the Eurozone, and the U.S.—are still in expansion mode. Moreover, the tariffs and the higher costs associated with them have continued to push up prices for consumers and producers. T. Rowe Price estimates that a 15% effective tariff rate will increase annual headline inflation by 1.0 and 1.6 percentage points per year. 1

This places the Fed in a difficult position, preventing action in either direction and keeping rates relatively stable. With that and these three factors in tow, Treasury yields should increase. With yields already above 4%, a 6% yield on the 10-year is truly possible.

Potential Implications of 6% Yields

So, if Treasury yields rise to 6%, what does it mean for our portfolios? In the short term, ample volatility. As bond yields rise, prices decline. For bonds already on the market, this means investors may incur heavy losses. This could be an issue, considering that fixed-income allocations and weightings have continued to grow post-pandemic as the various subsectors of the fixed-income universe are now paying yields unseen in decades.

But once we overcome that hurdle, we could witness a once-in-a-generation buying opportunity.

With yields on Treasury bonds reaching 6%, equities become less essential. After all, if equity-like returns are attainable without much equity risk, it is an obvious choice. Likewise, if the risk-free rate of return—i.e., Treasury yields—is higher, riskier bond types like junk bonds and corporates will also need to rise. Investors can essentially have portfolios of nearly all bonds and hardly any stocks to meet their goals.

Overall, the road to 6% Treasury yields is a potential game-changer for portfolio design.

Getting From Here To There

The question is, how do we position ourselves today to capitalize on the potential for much higher yields tomorrow? The answer may not be to bonds with longer maturities today. After all, these bonds and bond funds will see larger declines as yields rise to meet the new market risks. Investors buying today will expose themselves to volatility and losses unless they are willing to hold the bonds to maturity.

According to T. Rowe Price, the answer to the waiting game is to go short. Short-term bonds or those with near-term maturities—such as those between one year and 3.5 years—aren’t nearly as volatile as those with longer timelines. Because of their shorter timelines, short-term bonds have lower durations and can “roll over” faster than a 30-year bond. But yields are still ample in this fixed-income subsector. Investors can buy short-term bonds, collect good yields, and then reinvest the proceeds into higher-yielding treasuries in a few years.

T. Rowe Price also suggests adding inflation‑linked bonds and floating-rate debt that benefits from rising interest rates/yields.

Short-Term Bond ETFs

These ETFs are selected for their ability to tap short-term credit-duration bonds at a low cost. They are sorted by their year-to-date (YTD) total return, which ranges from 2.6% to 4.9%. Their expense ratio ranges from 0.03% to 0.55%. They have assets under management (AUM) ranging from $468 million to $58 billion. They are yielding between 2.4% and 7.6%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| IGSB | iShares 1-5 Year Investment Grade Corporate Bond ETF | $21.7B | 4.9% | 4.4% | 0.04% | ETF | No |

| DFSD | Dimensional Short-Duration Fixed Income ETF | $4.8B | 4.8% | 3.9% | 0.17% | ETF | Yes |

| SCHJ | Schwab 1-5 Year Corporate Bond ETF | $529M | 4.8% | 4.8% | 0.03% | ETF | No |

| VCSH | Vanguard Short-Term Corporate Bond ETF | $41.1B | 4.7% | 4.5% | 0.03% | ETF | No |

| FSIG | First Trust Limited Duration Investment Grade Corporate ETF | $1.3B | 4.5% | 4.54% | 0.55% | ETF | Yes |

| LDUR | PIMCO Enhanced Low Duration Active ETF | $989M | 4.5% | 4.7% | 0.51% | ETF | Yes |

| SLQD | iShares 0-5 Year Investment Grade Corporate Bond ETF | $2.3B | 4.3% | 4.2% | 0.06% | ETF | No |

| SPSB | SPDR Portfolio Short Term Corporate Bond ETF | $8.4B | 3.9% | 4.8% | 0.04% | ETF | No |

| SCHO | Schwab Short-Term U.S. Treasury ETF | $12.4B | 3.5% | 3.9% | 0.03% | ETF | No |

| SHY | iShares 1-3 Year Treasury Bond ETF | $26B | 3.4% | 3.8% | 0.15% | ETF | No |

| BSV | Vanguard Short-Term Bond ETF | $58B | 3.3% | 3% | 0.04% | ETF | No |

| SHM | SPDR Nuveen Bloomberg Short Term Municipal Bond ETF | $3.4B | 3.2% | 2.6% | 0.20% | ETF | No |

| CGSM | Capital Group Short Duration Municipal Income ETF | $709M | 2.9% | 3.6% | 0.25% | ETF | Yes |

| SHYG | iShares 0-5 Year High Yield Corporate Bond ETF | $6.5B | 2.9% | 7% | 0.30% | ETF | No |

| FSMB | First Trust Short Duration Managed Municipal ETF | $468M | 2.8% | 3.1% | 0.55% | ETF | Yes |

| SJNK | SPDR Bloomberg Short Term High Yield Bond ETF | $5B | 2.6% | 7.6% | 0.40% | ETF | No |

| SUB | iShares Short-Term National Muni Bond ETF | $9.9B | 2.7% | 2.4% | 0.07% | ETF | No |

| MEAR | BlackRock Short Maturity Municipal Bond ETF | $1.1B | 2.6% | 2.8% | 0.25% | ETF | Yes |

All in all, fiscal woes, rising inflation, and still-growing world economies are all reasons why Treasury yields could reach 6% over the next 18 months or so. For investors, this is a watershed moment. From that point on, fixed income could become the driver, while equities remain in the backseat. Until that point, investors should capitalize on strong yields in short-term bonds while awaiting higher-yielding long-term debt in the near future.

Bottom Line

Despite cutting rates, yields on Treasury bonds remain high and rising, and now, 6% is no longer out of the question. This scenario creates a fundamentally different portfolio landscape for investors, necessitating a major shift in our allocation strategy.

1 T. Rowe Price (2025-09). The greatest fixed income investment opportunity in decades?