Investors have had little chance to get comfortable lately. Equity markets have been driven by sharp rotations, geopolitical headlines, sticky inflation concerns, and shifting expectations around Federal Reserve policy. Bonds, which historically served as a stabilizing counterweight to equities, have experienced their own bouts of volatility as Treasury yields swung dramatically in response to inflation data, growth concerns, and changing rate expectations. This has created a difficult environment for portfolio construction—with investors still needing income, diversification, and ballast when equity volatility spikes.

That is helping drive renewed attention toward an often-overlooked segment of the bond market: taxable municipal bonds.

Long associated with institutional investors and less familiar than their tax-exempt counterparts, taxable munis have quietly become one of the more compelling fixed-income tools available today, combining strong credit quality, attractive yields, diversification benefits, and historically resilient performance during turbulent markets.

Taxable Municipal Bonds?

Most investors are familiar with traditional municipal bonds, issued by state and local governments to fund public projects, such as schools, roads, utilities, transportation infrastructure, and hospitals. The defining feature of traditional muni bonds is their tax-exempt status: interest paid on most munis is federal and, in some instances, state tax-free, making them a traditional haven for investors in higher tax brackets, endowments, and insurance pools.

What most investors may not realize is that a whole ecosystem of municipal bonds exists without the tax exemption. These bonds are still issued by municipalities and public entities, but the interest they pay is taxable at the federal and potentially state level. They are often issued for projects or structures that do not qualify for tax-exempt treatment, or when municipalities find it economically advantageous to issue taxable debt instead.

The taxable municipal bond market emerged after the Tax Reform Act of 1986 eliminated the ability for issuers to sell tax-exempt bonds for certain purposes. The 2017 Tax Cuts and Jobs Act then removed so-called prefunding and prohibited cities, states, and other municipalities from issuing tax-free bonds to restructure existing debts, further expanding the taxable muni market. Today, roughly $370 billion worth of taxable munis are outstanding, and issuance continues to rise.

High Quality Meets Attractive Income

Investors may be doing their portfolios a real disservice by ignoring this asset class, as taxable munis offer compelling benefits on several fronts.

Many investors initially question the income angle with taxable munis, since traditional tax-free munis tend to offer lower headline yields but a higher after-tax yield than many asset classes. The question is: why bother with taxable munis?

The reality is that taxable munis have yielded more than their tax-free counterparts over time. According to Charles Schwab, since January 2010, an index of taxable municipal bonds has yielded an average of 1.0% more than an index of tax-exempt municipal bonds. Today, investors can pick up about 1.2% more yield in taxable muni bonds. 1

Taxable munis also yield more than other fixed-income varieties. The Bloomberg Taxable Municipal Bond Index currently yields 4.94%, while the Bloomberg U.S. Aggregate Bond Index pays 4.57%, meaning taxable muni bonds offer extra income over the broader bond market.

That income also comes with high credit quality.

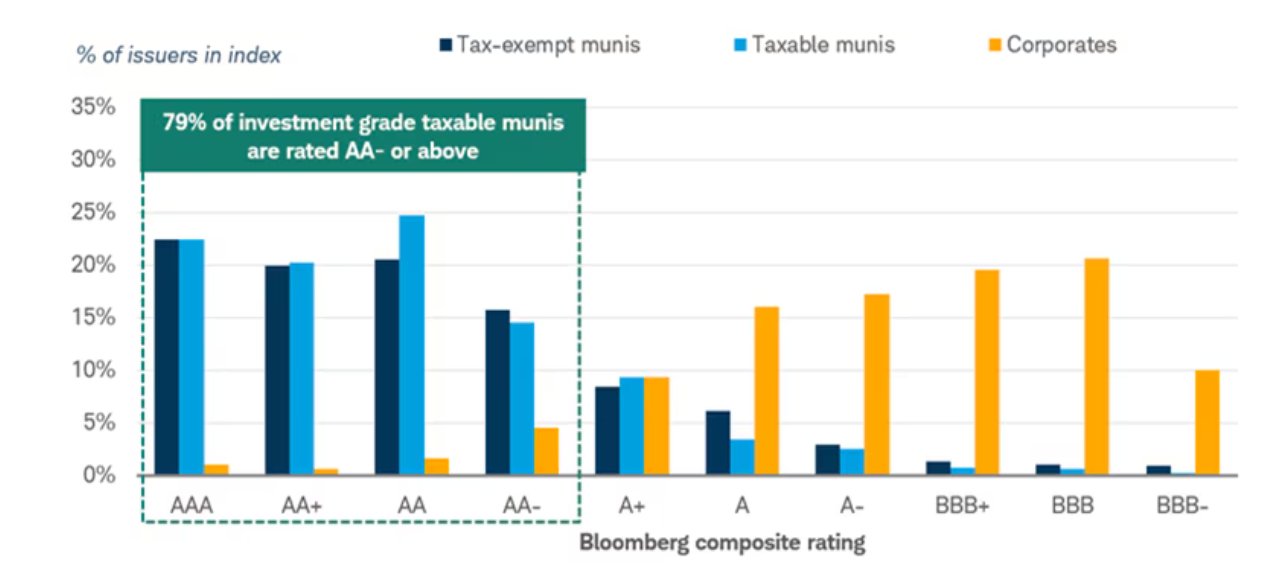

Compared to other forms of investment-grade debt, such as corporate bonds, munis win on the quality front. Issued by states and local municipalities with taxing authority, the vast bulk of taxable munis sit high on the credit ladder—roughly 79% of the taxable municipal market is rated AA minus or above, compared to just 8% for investment-grade corporate bonds. This chart from Charles Schwab underscores the sector’s high credit quality.

Source: Charles Schwab

This quality advantage also shows up in default rates. Historically, taxable munis have experienced far fewer defaults than investment-grade corporate bonds.

The low default rate and high yield have made taxable munis a better overall performer—with a 4.9% average total return—than corporate bonds (3.9%), Treasuries (2.0%), and even tax-free municipal bonds (3.2%) since 2010.

With taxable munis, investors get a strong-yielding bond with higher returns and investment-grade credit quality.

Perfect For Today's Environment

Given these benefits, taxable munis make a strong case for portfolio inclusion, particularly amid rising market volatility. They have historically shown attractive resilience during credit market stress, and because they occupy a unique niche—neither pure sovereign exposure nor traditional corporate credit—they can behave differently during market dislocations, exhibiting lower volatility than other investment-grade bonds and equities.

Adding a dose of taxable munis to a portfolio makes considerable sense.

The challenge lies in gaining exposure. While the surge in taxable muni issuance has put more of these bonds on the market, buying and selling them remains difficult, as with most municipal bonds. ETFs and closed-end funds (CEFs) remain the most effective approach, and some active muni managers also have the leeway to include taxable bonds in their portfolios.

Taxable Muni Bonds ETFs

These funds were selected based on their exposure to the taxable municipal and Build America bond sectors, sorted by YTD total returns ranging from -2.3% to 1.2%. Expenses range from 0.28% to 2.63%, assets under management fall between $367 million and $1.53 billion, and current yields range from 4.1% to 10.05%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| BAB | Invesco Taxable Municipal Bond ETF | $1.53B | 1.2% | 4.1% | 0.28% | ETF | No |

| GBAB | Guggenhm Txble Mcpl Bnd and Invt Gd Dt Trt | $367M | -0.8% | 10.05% | 1.34% | CEF | Yes |

| BBN | Blackrock Taxable Municipal Bond Trust | $1.11B | -2% | 7.4% | 1.84% | CEF | Yes |

| NBB | Nuveen Taxable Municipal Income Fund | $499M | -2.3% | 7.5% | 2.63% | CEF | Yes |

Market volatility has reminded investors that diversification still matters—and that not all fixed-income sectors offer the same balance of risk and reward.

Taxable municipal bonds stand out by combining the characteristics investors want during uncertain periods: high credit quality, attractive income, diversification, and relative resilience.

Bottom Line

In a world where traditional fixed-income sectors increasingly come with tradeoffs, taxable munis offer a differentiated and compelling alternative. For investors seeking income without excessive credit risk—and stability without sacrificing yield—this often-overlooked corner of the bond market deserves much closer attention.

1 Charles Schwab (April 2026). Things to Consider About Taxable Municipal Bonds