Income investing has become considerably more attractive over the past several years. Rising interest rates have lifted yields across virtually every corner of the fixed-income market, allowing investors to generate income levels that were nearly impossible during the decade following the Global Financial Crisis. However, higher yields have come with higher uncertainty, as inflationary trends, ambiguity about the Fed’s path, and mixed economic data have muddied the waters. For many investors, the challenge has become finding an asset class that offers attractive yields without taking on excessive default risk.

One area that increasingly stands out is the high-yield municipal bond market.

Although many investors associate municipal bonds with conservative, investment-grade income, the high-yield municipal sector tells a different story. These bonds often provide yields comparable to or even exceeding traditional corporate junk bonds while historically experiencing dramatically lower default rates. Add in the potential for federal tax-exempt income, and the sector begins to look increasingly attractive for investors seeking both income and risk-adjusted returns.

High-Yield Municipal Bonds?

Arguably, the $4.5 trillion municipal bond market is one of the most misunderstood sectors in fixed income. Many investors- even sophisticated institutional ones- tend to paint the muni market with a broad-brush stroke. That’s a real shame, as various pockets of the sector offer different yield and return potential. One of which is the high-yield market.

Like traditional general obligation (GO) bonds, high-yield municipal bonds are issued by public authorities. The difference is that these bonds expand this definition beyond state and local governments to include nonprofit organizations, hospitals, universities, transportation systems, airports, charter schools, and other public-purpose entities. And more often than not, these bonds are issued to fund a specific project.

The bonds are repaid by the revenues generated from the project. Therefore, as people use the funded hospital, mass transit system, utility, or sports stadiums/concert venue, a portion of the cash is used to pay off the bondholders. This is a key distinction vs. GO bonds, which are paid via tax revenues.

Attractive Income With Tax Advantages

This distinction creates an interesting advantage for investors. Because the repayment is derived from the usage of the underlying project, there is some risk of non-repayment. In theory, the State of Texas could tax its residents 100% to pay off one of its GO bonds. Not so for a new toll road. Therefore, they receive lower credit ratings because they finance projects with unique revenue streams, limited operating histories, or specialized purposes rather than because they face imminent financial difficulty.

Therefore, revenue-backed munis often come with higher yields than traditional GO bonds and have lower credit ratings. Investors simply want more yield to compensate for the added risk.

And with lower and potentially less-than-investment-grade credit ratings, they are often given the “junk” moniker. Unlike corporate junk bonds, though, a municipal bond does not necessarily mean high yield because the issuer is financially distressed. In fact, it’s quite the opposite.

When looking at default rates, high-yield munis have exhibited way lower defaults than their corporate twins.

According to Lord Abbett, when looking at cumulative default rates over a rolling 10-year period from 1970 to 2024, high-yield munis have experienced a 6.69% default rate. This compares to a 29.71% default rate for corporate junk bonds. Additionally, high-yield munis have offered a much higher recovery rate for investors after the defaults than junk corporate bonds. Remember, these are bonds tied to assets. Stadiums, hospitals, and public utilities still have value. 1

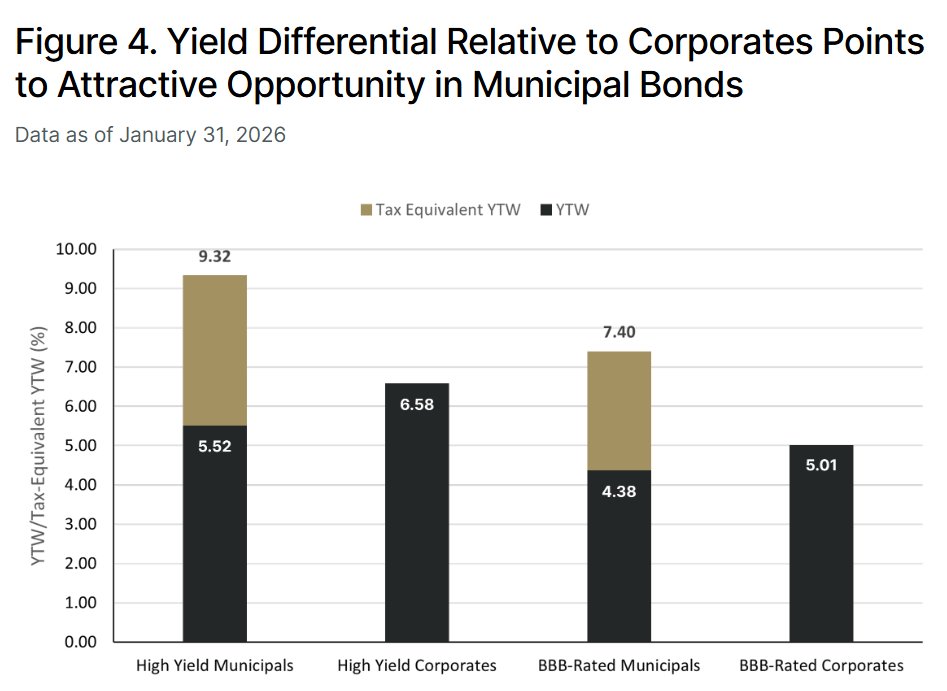

What’s particularly interesting amid these lower default rates is that high-yield munis may offer a better yield.

Just like traditional and investment-grade muni bonds, interest income generated by high-yield municipal bonds is generally exempt from federal income taxes and, in some cases, state and local taxes as well. The taxable-equivalent yield can therefore become substantially higher than the stated yield, as much as 3%.

This chart from Lord Abbett underscores the yield differential in high-yield munis over high-yield corporate bonds for someone in the highest tax brackets. The best part, an investor in the low 22% still makes out in yield in junk munis versus corporate bonds.

Source: Lord Abbett

Today’s market environment only strengthens the investment case for high-yield munis.

Corporate high-yield spreads have compressed considerably following recent market rallies.

While nominal yields remain attractive, investors are receiving less incremental compensation for assuming additional corporate credit risk than they have during many previous market cycles. At the same time, economic uncertainty continues to increase. Slower growth, elevated borrowing costs, refinancing pressures, and changing consumer demand all create challenges for lower-rated corporate borrowers. Essentially, investors are getting less after-tax yield for more risk.

According to Lord Abbett, high-yield municipals have historically delivered attractive risk-adjusted returns because investors receive relatively generous income while benefiting from lower default experience than traditional high-yield corporate debt. That combination becomes particularly attractive during periods of economic uncertainty like today.

ETFs Have Made the Sector More Accessible

For many investors, balancing the need for high income amid a world of rising risks means that high-yield and revenue-backed municipal bonds could be the best “junk” bond to buy. Ultimately, they’ll get a lower default rate coupled with strong income potential.

Historically, investing in high-yield municipal bonds was a tough hill to climb, which helps explain why many investors have traditionally ignored the sector. To own them, investors need a large capital base to purchase individual bonds, must accept wide bid/ask spreads if the bonds trade at all, or must work through costly specialized municipal bond managers.

Today, ETFs have dramatically expanded access.

Investors can choose from diversified high-yield municipal bond ETFs that provide exposure across hundreds of issuers while maintaining daily liquidity and relatively low costs. Both passive and actively managed ETFs now serve the marketplace, with ample options covering various durations within the high-yield muni space. For many investors, ETFs have become the easiest way to incorporate high-yield municipal exposure into broader fixed-income allocations.

High-Yield Municipal Bond ETFs

These funds were selected based on their exposure to the high-yield municipal bond market. Sorted by YTD total return, they range from 2.8% to 7.8%, with assets under management between $82M and $2.92B, expense ratios between 0.32% and 1.82%, and current yields between 1.8% and 4.9%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| XMPT | VanEck CEF Muni Income ETF | $239M | 7.8% | 5.7% | 1.82% | ETF | No |

| HYMU | BlackRock High Yield Muni Income Bond ETF | $82M | 5.1% | 4.3% | 0.35% | ETF | No |

| HYMB | SPDR® Nuveen Bloomberg High Yield Municipal Bond ETF | $2.59B | 4.3% | 4.2% | 0.35% | ETF | No |

| FMHI | First Trust Municipal High Income ETF | $573M | 4.3% | 4% | 0.70% | ETF | Yes |

| JMHI | JPMorgan High Yield Municipal ETF | $175M | 3.8% | 4.9% | 0.49% | ETF | Yes |

| HYD | VanEck High Yield Muni ETF | $2.92B | 3.6% | 4.3% | 0.32% | ETF | No |

| SHYD | VanEck Short High Yield Muni ETF | $329M | 2.8% | 3.3% | 0.35% | ETF | No |

The search for income has grown increasingly complicated. Investors want higher yields but recognize that today’s economic environment presents meaningful risks for lower-quality borrowers. Traditional corporate high-yield bonds remain an important part of the fixed-income universe, but tighter credit spreads and growing economic uncertainty have led many investors to question whether they are being adequately compensated for the risks they assume.

High-yield municipal bonds offer a compelling alternative.

Despite carrying below-investment-grade ratings, they have historically experienced significantly lower default rates than corporate junk bonds while delivering attractive income and valuable tax advantages. In an environment where every basis point of yield matters and every source of risk deserves scrutiny, high-yield municipals may prove to be the smarter alternative to traditional junk bonds.

Bottom Line

For investors seeking to maximize after-tax income while maintaining a focus on risk-adjusted returns, high-yield municipal bonds may represent one of today’s most overlooked opportunities.

1 Lord Abbett (April 2026). High Yield Municipal Bonds: An Attractive Choice for Risk-Adjusted Return