There’s an old investing adage that says, “It’s not what you earn, it’s what you keep.” Thanks to $0 trading commissions, direct indexing, and exchange-traded funds (ETFs), tax-loss harvesting has quickly emerged as a way for investors to reduce what they owe the U.S. government and potentially boost their after-tax returns. However, tax-loss harvesting is often discussed in the context of equities.

Investors in fixed‐income portfolios are increasingly recognizing that the strategy also holds significant potential in the bond market.

For fixed-income investors, especially those in taxable accounts, realizing intentional losses can meaningfully drive after-tax returns and portfolio efficiency. In an environment characterized by volatile interest rates, widening credit spreads, and shifting liquidity conditions, the opportunity set for tax-loss harvesting in bonds may be powerful.

What Is Tax-Loss Harvesting?

At its core, tax‐loss harvesting is the practice of selling securities that have incurred capital losses, where the cost basis exceeds current market value. While that may seem counterintuitive, it can provide a portfolio with ample benefits.

For starters, those losses may be used to offset realized capital gains elsewhere in the portfolio. This reduction can be significant, especially if the gains are considered short-term and taxed at ordinary income rates as high as 37%.

Even better, those losses can be reduced to your ordinary income. If your capital losses exceed the gains, or if you have no capital gains in a year, $3,000 worth of those losses can be used to reduce your ordinary income. And if you lose more than $3,000 on a stock, the excess can be pushed into the future to offset capital gains and ordinary income later on. For investors across various tax brackets and income levels, prudent tax-loss harvesting can significantly enhance returns.

Asset manager Parametric estimates that portfolio tax management can add 1% to 2% in after-tax excess returns for a portfolio. 1

Bonds Get In On The Act

Most investors have focused their tax-loss harvesting on the equity side. After all, stocks tend to be more volatile than bonds. Additionally, the sheer breadth of the bond universe, issues of liquidity, tax‐lot complexity, and the lower turnover typical of bond funds made it more difficult to harvest losses in bonds than equities.

But that was yesterday, and this is today. Tax-loss harvesting works well for bonds. Parametric reveals that successful tax-loss harvesting can add 0.3% to a fixed-income portfolio. While that may not seem like much, it is. Bond investing is a game of inches, and that is meaningful additional return. Remember, the broader bond market yields about 4%.

Moreover, the volatility of the bond market is now growing. Despite being called fixed income, there’s not too much in the way of being “fixed” about bonds, at least when it comes to price. Over the past few years, rising interest rates have inflicted significant capital declines across a wide range of fixed-income sectors. At the same time, fiscal uncertainty, trade complications/tariffs, and news reactions have only increased bond market volatility. The so-called MOVE Index—which measures bond market volatility—remains at elevated levels.

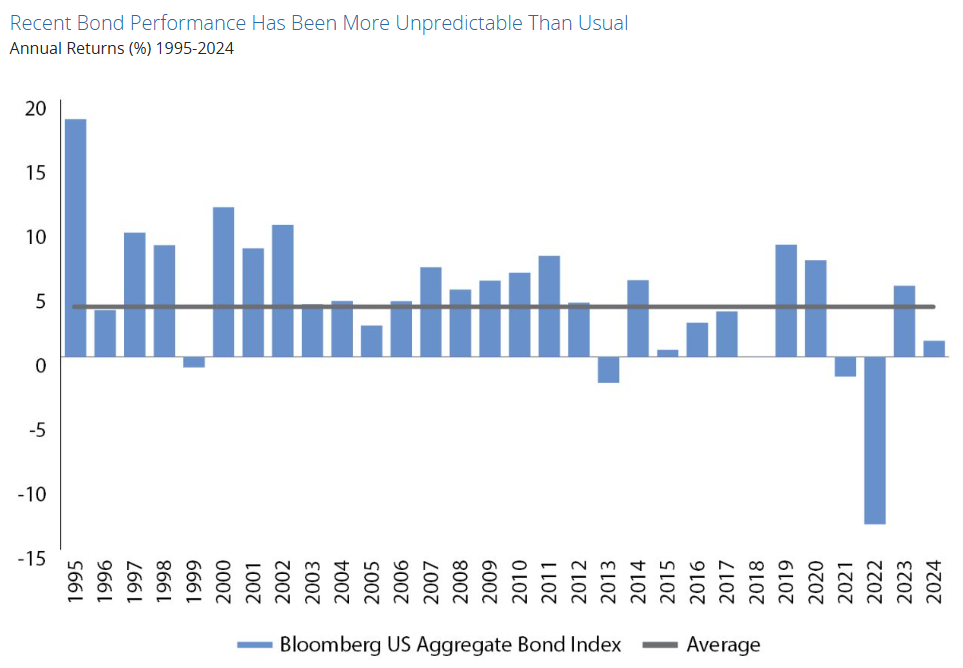

This chart from Hartford Funds reveals just how wide a range of returns the broader Bloomberg Agg Index has seen over the last few decades. Moreover, examining the bonds within the index reveals a wide range of returns and losses.

Source: Hartford Funds

That volatility is ripe for tax-loss harvesting within the bond sector. By exploiting the volatility throughout the year, investors can gain valuable tax benefits and additional alpha.

Time To Tax-Loss With Bonds Too

After several years of unpredictable bond performance, now may be a particularly fruitful time for tax-loss harvesting in fixed income. Ultimately, investors can shift around their portfolios and capitalize on the potential.

The key to making this work is harvesting losses and then tax swapping.

Harvesting is the act of selling your losers to book the losses for tax purposes. The swap piece is finding a replacement for the proceeds. When a bond is sold at a loss, the proceeds can be redeployed into another bond or fund with similar risk and return characteristics, thereby maintaining portfolio exposure while resetting cost basis. You could sell an individual corporate bond and buy a corporate bond ETF. Swap out a treasury-focused fund for a broader investment-grade credit ETF or muni bond ETF.

This can be particularly powerful in a rising‐rate environment, where older bonds with lower coupons have fallen in value. Investors can lock in higher yields in similar credit-rated bonds with higher yields.

Popular Bond ETFs

These ETFs were selected based on their low-cost exposure to core bonds, Treasuries, investment-grade corporate bonds, and mortgage-backed securities. They are sorted by their YTD total return, which ranges from -0.5% to 0.6%. They have expense ratios between 0.03% and 0.36% and assets under management between $55 million and $314 billion. They are currently yielding between 3.6% and 4.8%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| VCIT | Vanguard Intermediate-Term Corporate Bond Index Fund | $57B | 9.1% | 4.8% | 0.03% | ETF | No |

| LQD | iShares iBoxx $ Investment Grade Corporate Bond ETF | $31.8B | 8.2% | 4.3% | 0.14% | ETF | No |

| AVIG | Avantis Core Fixed Income ETF | $1.3B | 7.9% | 4.3% | 0.15% | ETF | Yes |

| HCRB | Hartford Core Bond ETF | $346M | 7.8% | 4.3% | 0.29% | ETF | Yes |

| USHY | iShares Broad USD High Yield Corporate Bond ETF | $25B | 7.7% | 6.8% | 0.08% | ETF | No |

| VCRB | Vanguard Core Bond ETF | $3.13B | 7.6% | 4.4% | 0.10% | ETF | No |

| IUSB | iShares Core Total USD Bond Market ETF | $33.1B | 7.4% | 4.2% | 0.07% | ETF | No |

| SPAB | SPDR® Portfolio Aggregate Bond ETF | $8.68B | 7.4% | 4% | 0.03% | ETF | No |

| AGG | iShares Core U.S. Aggregate Bond ETF | $132B | 7.3% | 3.9% | 0.03% | ETF | No |

| BND | Vanguard Total Bond Market Index Fund | $360B | 7.2% | 3.9% | 0.03% | ETF | No |

| FIGB | Fidelity Investment Grade Bond ETF | $254M | 7.1% | 4% | 0.36% | ETF | Yes |

| TLT | iShares 20+ Year Treasury Bond ETF | $48.8B | 6.9% | 4.3% | 0.15% | ETF | No |

| GBF | iShares Government/Credit Bond ETF | $137M | 6.8% | 3.8% | 0.20% | ETF | No |

| SJNK | SPDR Bloomberg Short Term High Yield Bond ETF | $5B | 6.5% | 6.8% | 0.40% | ETF | No |

| VCSH | Vanguard Short-Term Corporate Bond Index Fund | $46B | 6.2% | 4.5% | 0.03% | ETF | No |

| BSV | Vanguard Short-Term Bond Index Fund | $65.5B | 5.7% | 4% | 0.03% | ETF | No |

| SHY | iShares 1-3 Year Treasury Bond ETF | $24B | 4.6% | 3.8% | 0.15% | ETF | No |

Tax‐loss harvesting in fixed income is far from a mere technical tax planning exercise. When executed thoughtfully, it can become an integral part of a bond investor’s growth of after-tax return. With the growth of ETFs and other vehicles, it’s easy for bond investors to enjoy additional returns by effectively tax-loss harvesting their portfolios.

Bottom Line

For advisors and individual investors alike, the time is ripe to treat tax-loss harvesting not as an afterthought, but as a strategic lever within fixed‐income portfolio construction. Ultimately, the strategy works well for bonds and can enhance returns to a portfolio.

1 Parametric (2025-04). Fixed Income Tax Loss Harvesting: Realizing Losses No Matter When They Occur