For much of the past few decades, bonds have served as a cornerstone of diversified portfolios. They once provided reliable income, ballast against equity volatility, and refuge during equity downturns. This pattern held last year, as many bond investors enjoyed strong total returns from high starting yields and falling rates that boosted prices. That backdrop restored faith in bonds after years of low or negative real returns, and many investors carry that optimism into 2026.

Yet structural and economic risks beneath this attractiveness may make bonds less appealing than they appear.

In fact, some leading strategists now warn that bonds may no longer serve as a haven and that alternatives could outshine traditional fixed-income strategies. As investors consider new-year allocations, they should examine not only why bonds have recently been favored but also why they may not be the best bet going forward.

Bonds' Recent Appeal

The bond market has shifted from pariah to top investment destination for portfolios. The so-called excellent Reset in post-pandemic years has structurally reorganized the sector and restored its mojo.

First, yields across government, investment-grade, and even high-yield corporate bonds rose significantly during the rate-hiking cycle in response to inflation and monetary tightening. For the first time in years, investors could earn meaningful income from fixed-income instruments without extreme credit risk.

Second, with inflation moderating from multi-decade highs and central banks—including the Federal Reserve—signaling a shift toward easing, policy, and falling interest rates added a second pillar of support. When rates fall, bond prices rise and provide capital gains alongside coupon income.

That dual potential from yields and gains lifted fixed-income performance in 2025.

Indeed, 2025 return data showed that broad bond indexes—including core and high-quality bonds—posted solid gains, largely from coupon income and a modest rally in longer yields. Overall, the benchmark Bloomberg U.S. Aggregate Bond Index delivered a roughly 7% total return—the best since 2020. Several riskier segments, such as emerging market bonds, doubled that return.

Bonds Could Be Riskier Than They Appear

After any asset class enjoys a strong year, investors must re-evaluate whether gains can repeat. While bonds hold intuitive appeal, several risks suggest their 2026 attractiveness may be more myth than momentum.

For starters, elevated default and credit stress risks now threaten fixed income. Fixed income assumes stable or improving credit quality, yet rising defaults—especially in lower-rated corporate debt—endanger bond returns. Corporate leverage remains historically high after years of low interest rates and extensive borrowing.

Now, the leverage’s effects are emerging. For example, First Brands Group’s bankruptcy, subprime auto lender Tricolor’s receivable-backed woes, and Blue Owl’s software-focused bond issues represent recent headline defaults. Ratings agency Fitch notes that private credit defaults reached 5.8% in early 2026, above averages. 1

And while those notable defaults occurred in private credit, slowing or stagnant economic growth could make weaker issuers struggle to service debt, potentially raising default rates across the board.

Second, bread-and-butter government bonds have long been the quintessential safe asset, yet this assumption now faces challenges. The United States continues to run substantial budget deficits, and expanding government debt supply may weigh on prices and yields if demand lags. We have seen this in action: despite rate cuts—which should lower yields—investors still demand more from longer-dated bonds.

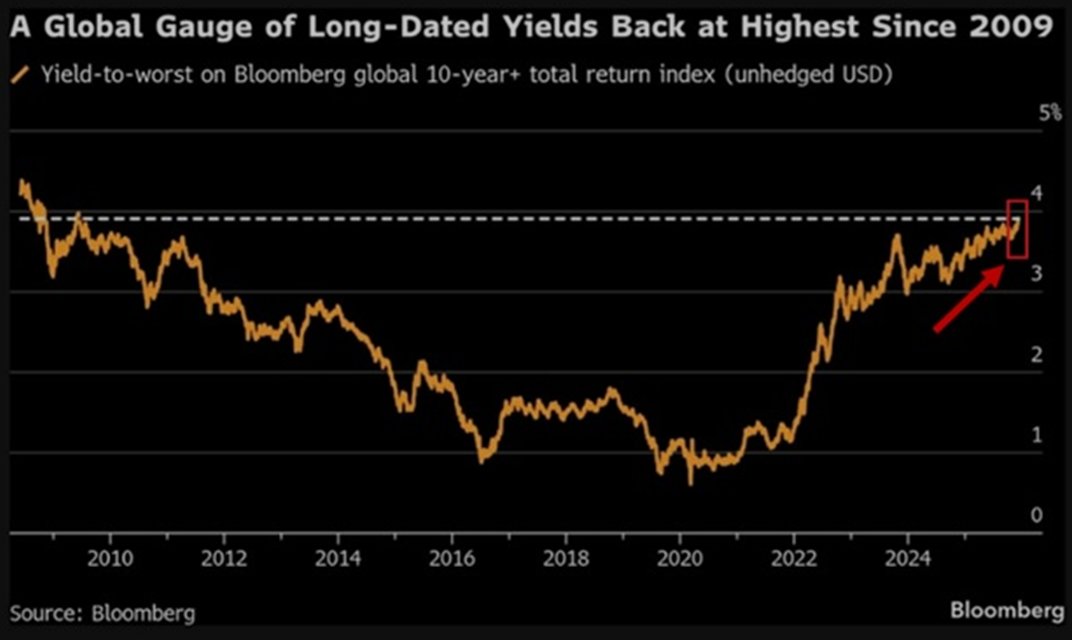

And it’s not just domestic. Investors continue reassessing long-dated maturities from various sovereign nations. This chart from Bloomberg illustrates investors worrying about the world’s rising debt crisis over the long term, reflected in higher yields.

Source: Bloomberg

Overall, market reactions suggest long-dated Treasuries may prove less reliable as equity market hedges than in prior decades.

Then there’s an old foe: inflation. Though inflation has moderated from recent peaks, many pressures could prove more durable than policymakers or investors expect. Structural forces like supply-chain reconfiguration, geopolitical fragmentation, and labor market tightness may keep core inflation elevated. We have already seen this in effect.

Data illustrates the 12-month change in headline Consumer Price Index (CPI) has held between 2.3% and 3.5% since early 2024. Absent a slight November moderation, CPI stayed between 2.8% and 3.4% for 17 straight months.

If inflation remains stubborn and fails to return to central-bank targets as quickly as hoped, real yields could stay unattractive or turn negative in real terms. Bonds may then fail to provide the capital preservation investors seek, especially if rate cuts prove less aggressive than anticipated or if inflation expectations rise. Some strategists expect only limited rate cuts in 2026, which may not sufficiently lift bond valuations.

The “Anything But Bonds” Narrative

With that, prominent strategists now openly question bonds’ portfolio role. For example, Bank of America chief equity strategist Michael Hartnett recently captured this sentiment in client commentary, proposing “anything but bonds” as the theme for the decade’s remainder.

Bonds’ added risks warrant consideration—what should investors do? Liquid alts offer a potential answer.

Liquid alts encompass diverse assets and strategies designed to deliver returns across market conditions, from familiar ones like real estate, gold, and currencies to exotic ones like managed futures, options strategies, long-short, and event-driven trading.

Most liquid alts belong to so-called absolute return funds, designed to produce returns year in and year out. Those returns resemble base hits rather than home runs, and that consistency makes alts suitable as bond replacements and portfolio anchors.

Investors may not want to eliminate all bond exposure, but they could benefit from alternatives as bond market risks rise and returns from the asset class potentially decline.

Alternatives ETFs

These funds, selected for their access to liquid alternatives across various strategies, are sorted by YTD total return from -3.2% to 7.7%. Expense ratios range from 0.35% to 1.38%, with AUM between $150M and $40B. They currently yield between 1.7% and 14.1%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| RLY | SPDR SSgA Multi-Asset Real Return ETF | $486M | 7.7% | 7.5% | 0.50% | ETF | No |

| QAI | IQ Hedge Multi-Strategy Tracker ETF | $695M | 2.2% | 2.3% | 1.13% | ETF | No |

| JEPI | JPMorgan Equity Premium Income ETF | $40.2B | 2% | 11.5% | 0.35% | ETF | Yes |

| WTMF | WisdomTree Managed Futures Strategy Fund | $185M | 1.6% | 1.7% | 0.65% | ETF | Yes |

| FTLS | First Trust Long/Short Equity ETF | $1.95B | -0.1% | 1% | 1.38% | ETF | Yes |

| JEPQ | JPMorgan Nasdaq Equity Premium Income ETF | $23.4B | -0.3% | 14.1% | 0.35% | ETF | Yes |

| DBMF | iMGP DBi Managed Futures Strategy ETF | $1.38B | -2.5% | 2.9% | 0.85% | ETF | Yes |

| FMF | First Trust Managed Futures Strategy Fund | $157M | -3.2% | 2.1% | 1.01% | ETF | Yes |

Bonds have played a vital role in portfolios for decades, offering income, diversification, and a hedge against equity downturns. Strong returns in 2025 reinforced this reputation for many investors.

As 2026 progresses, the narrative shifts. Structural risks like rising defaults, elevated government debt, and potential inflation persistence suggest bonds may not be the safe bet many investors assume, making alternatives key.

Bottom Line

Bonds have benefited from high starting yields and recent rate relief, but mounting risks—from rising defaults and persistent inflation to growing U.S. fiscal pressures—suggest fixed-income offers less safety and upside than many expect. Diversification beyond traditional bonds grows vital in the year ahead.

1 Fitch Ratings (February 2026). U.S. Private Credit Default Rate Continues Upward March to 5.8% in January 2026