Over the past decade, private credit has captured the imagination of investors around the world. Once a niche corner of the market, it has grown into a massive asset class, fueled by institutional demand for higher yields and diversification away from traditional fixed-income. The appeal is easy to understand. Private credit funds often advertise higher yields, floating-rate structures, and the promise of stable returns with lower volatility. For many investors, particularly institutions, it has become a core allocation.

As the asset class has grown, so too have the risks. What was once a relatively conservative lending space has expanded into more complex and, in some cases, riskier areas. In particular, increasing exposure to start-up technology and software companies—often highly leveraged and dependent on optimistic growth assumptions—has begun to raise concerns.

At the same time, another segment of the market is quietly offering compelling opportunities: traditional high-yield and junk bonds. With lower exposure to A.I. and tech start-ups, the junk bond market is surprisingly well-suited for investors seeking high yields outside the private credit and A.I. mess.

Private Credit Faces Challenges

The beauty of private credit is that it’s, well, private. These loans are made outside public markets and are often structured directly between lenders and borrowers or through pooled investment vehicles, which is what makes the asset class appealing in the first place. This lack of liquidity helps the sector produce above-average yields, while the absence of daily trading is supposed to reduce volatility. Investors buy and hold these investments for the full market cycle, recovering their premium at the end.

For a massive endowment with billions in assets, this isn’t much of an issue. However, even for mid-sized portfolios, the lack of liquidity is becoming a major thorn in the asset class’s side, especially as the underlying loans have begun to run into trouble—and that is exactly what is happening today.

Concerns about artificial intelligence (AI) stocks, software, and technology start-ups—huge issuers of private credit loans—have started to impact the sector. Large defaults and write-downs have already emerged. For example, business development company BlackRock TCP Capital Corp recently wrote several loans down to $0, reducing its NAV by over 19%. The firm was not alone, as several other major private credit managers also wrote down the values of their software-related loans.

Looking ahead, the damage from software-related defaults in private credit could be growing.

Morgan Stanley expects annual private credit defaults of 8% between the second half of 2026 and the first half of next year. UBS analysts estimate that under a worst-case scenario, defaults could reach as much as 15%. Refinancing difficulties and a shortage of new investors willing to lend to software firms will drive the spike in defaults.

Junk Bonds Are Surprisingly Immune

While the private credit markets grow dicey, the traditional public high-yield market appears as steady as government debt. Despite carrying the “junk” label, the asset class has performed well amid the software woes that have rattled private credit. Junk bond yields are currently 2.81% higher than U.S. Treasury bond yields—below the historical average spread of 5.23% in extra yield.

The question is why. If other assets made to risky borrowers are suffering, why hasn’t junk responded in the same way?

It turns out there is very little software and A.I. exposure inside the junk bond universe.

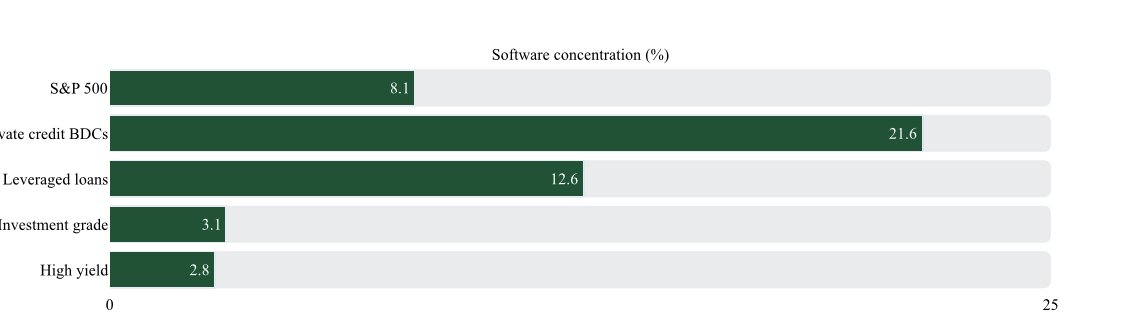

According to Insight Investment, a Bank of New York/Mellon subsidiary, roughly 1% of the U.S. high-yield market consists of issuers in cloud computing, semiconductors, or digital infrastructure for A.I. workloads. Businesses that have increasingly pivoted toward A.I.-related products and services comprise another 2.5%. For context, that is less direct exposure to these firms than the S&P 500 at 43% or even investment-grade bonds at nearly 17%. 1

When comparing junk bonds with private credit on overall software exposure—not just A.I. and SaaS firms—high yield again has the lowest exposure. The asset manager’s chart shows that leveraged loans and private credit BDCs carry the true concentration.

Source: Insight Investment

Junk simply does not have the kind of exposure to warrant A.I. or software default concerns.

Junk bonds may also offer better credit quality than private credit at this point. According to Insight Investment, the share of BB-rated bonds—the highest tier within the high-yield spectrum—has risen meaningfully over time, while the proportion of deeply distressed CCC-rated debt has generally declined outside of recessionary spikes. The share of top-tier non-investment-grade bonds has grown from 34% to 55% over the past 25 years, while the lowest-rated debt now makes up just 12% of the index.

Where have all the riskier borrowers gone?

Insight’s data shows they have migrated into the private credit and leveraged loan market. Because private credit specializes in bespoke financing for leveraged transactions, middle-market companies, and issuers that may not meet the disclosure, scale, or liquidity requirements of public bond markets, it has siphoned off the riskier borrowers, improving the overall quality of the junk bond market.

Why Investors May Prefer High Yield Today

High-yield bonds offer a more straightforward and transparent way to access income and credit exposure, providing many of the benefits investors seek—such as yield and diversification—while avoiding the challenges of private markets. Given lower default risks relative to private credit, traditional high-yield bonds may represent a more appealing alternative, particularly for investors concerned about rising defaults in technology-focused lending or the constraints of illiquid investments.

Gaining exposure is easy thanks to the rise of ETFs. While buying individual junk bonds can be difficult, the growth of both passive and active ETFs has made adding high-yield bond exposure as simple as clicking a mouse.

Passive Junk Bond ETFs

These funds provide junk bond exposure and yields, sorted by 1-year total return from 6.7% to 6.9%. Expense ratios range from 0.05% to 0.49%, AUM from $3.9 billion to $24 billion, and current yields from 5.7% to 7.3%.

| Ticker | Name | AUM | 1-year Total Ret (%) | Yield | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| USHY | iShares Broad USD High Yield Corporate Bond ETF | $23.8B | 6.9% | 6.9% | 0.08% | ETF | No |

| HYG | iShares iBoxx $ High Yield Corporate Bond ETF | $17.4B | 6.8% | 5.7% | 0.49% | ETF | No |

| JNK | SPDR Bloomberg High Yield Bond ETF | $7.9B | 6.8% | 6.5% | 0.40% | ETF | No |

| HYLB | Xtrackers USD High Yld Corporate Bd ETF | $3.93B | 6.8% | 6.6% | 0.05% | ETF | No |

| SPHY | SPDR Portfolio High Yield Bond ETF | $8.7B | 6.7% | 7.3% | 0.05% | ETF | No |

Active Junk Bond ETFs

These actively managed funds provide high-yield bond exposure, sorted by 1-year total return from 1.3% to 4.7%. Expense ratios range from 0.22% to 1.02%, AUM from $50M to $5.63B, and current yields from 5.7% to 8.6%.

| Ticker | Name | AUM | 1-year Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| FLHY | Franklin High Yield Corporate ETF | $268M | 4.7% | 5.7% | 0.40% | ETF | Yes |

| YLD | Principal Active High Yield ETF | $160M | 4.7% | 7.2% | 0.39% | ETF | Yes |

| HYBL | SPDR Blackstone High Income ETF | $136M | 4.4% | 8.2% | 0.70% | ETF | Yes |

| THYF | T. Rowe Price U.S. High Yield ETF | $50M | 4.1% | 7.5% | 0.56% | ETF | Yes |

| SRLN | SPDR Blackstone Senior Loan ETF | $5.63B | 3.8% | 8.6% | 0.70% | ETF | Yes |

| FTSL | First Trust Senior Loan Fund | $2.27B | 3.8% | 7.5% | 0.87% | ETF | Yes |

| BKHY | BNY Mellon High Yield Beta ETF | $292M | 3.4% | 6.9% | 0.22% | ETF | Yes |

| PHYL | PGIM Active High Yield Bond ETF | $124M | 3.4% | 8.2% | 0.39% | ETF | Yes |

| HYFI | AB High Yield ETF | $123M | 3.4% | 6.7% | 0.40% | ETF | Yes |

| HYLS | First Trust Tactical High Yield ETF | $1.43B | 1.3% | 6.4% | 1.02% | ETF | Yes |

Public high-yield bonds, often overshadowed by private markets, offer a combination of transparency, liquidity, diversification, and income that is difficult to ignore. Their lower exposure to the most problematic areas of private credit—particularly technology-focused lending—positions them well for the current environment.

In a world where investors are increasingly focused on risk as well as return, the case for high-yield bonds is strengthening.

Bottom Line

In a market shaped by AI enthusiasm and growing concerns around tech-driven credit risk, public high-yield bonds offer a compelling alternative. With greater transparency, stronger diversification, and less exposure to vulnerable software-heavy borrowers, high yield delivers attractive income without many of the structural risks found in private credit.

1 Insight Investment (March 2026). Systematic Insights: Is high yield at less risk from AI?