It’s finally here. The interest-rate landscape is entering a new phase, with the Federal Reserve finally beginning to move on benchmark rates. After an extended period of aggressive rate hikes aimed at controlling inflation and cooling the economy, policymakers around the world appear increasingly poised to shift to rate cuts. For investors, this transition raises important questions about positioning, particularly within income-oriented asset classes.

Closed-end funds (CEFs), with their distinctive structure, use of leverage, and high-income potential, are susceptible to rate cycles and could be a big winner as the Fed finally starts seriously cutting rates.

While rising rates over the past few years created headwinds for many CEFs, a rate-cutting cycle can reverse much of that pressure. In this regard, the fund vehicle may benefit in ways that traditional mutual funds and exchange-traded funds (ETFs) cannot fully replicate. For portfolios, capturing these dynamics could provide plenty of upside in the new lower-rate environment.

All About Yield & Leverage

One of the key features of CEFs is their IPO structure. Unlike ETFs and mutual funds, which allow daily redemptions, CEFs are “closed.” And with that, CEFs maintain a stable pool of capital. This structure enables them to invest in less liquid asset classes and engage in buy-and-hold decisions. This also allows them to employ leverage on those assets.

Many CEFs borrow at short-term institutional rates, such as through preferred shares, credit facilities, or tender-option bond financing. They then invest the borrowed capital in longer-duration or higher-yielding assets. This spread – or the difference between what they earn in yield and what they pay in interest- drives additional yields and income for their shareholders. It’s why CEFs tend to yield more than a comparable ETF or mutual fund in the same asset class.

The issue is that during rate increase cycles, this leverage can hurt a CEF’s performance in two major ways.

For starters, when rates rise, short-term borrowing costs rise quickly. It becomes more expensive to borrow money. That added expense for a CEF reduces distribution coverage. There’s simply less spread to go around. And in some cases, it can evaporate all the extra yield that leverage can provide. This dynamic played out notably during the 2022–2023 rate-hiking cycle, when many CEFs saw borrowing costs rise by several percentage points. As a result, several highly leveraged funds cut their distributions.

Secondly, rising rates make less risky asset classes more advantageous. As rates rise, short-term instruments and safe assets like T-bills, certificates of deposits, money market funds, and even savings accounts pay high interest. Why take the risk when you can earn 4%+ in cash? As a result, investors tend to sell CEFs and move from the additional leverage risks and security risks within the vehicle.

A Reversal Of Fortunes

But the same structure that hurts CEFs in a rising-rate cycle can become a powerful tailwind when rates begin to fall. As short-term rates decline, the cost of leverage drops as well, and the income-generation engine of a CEF becomes significantly more efficient. This is where the rate-cut cycle begins to shift the narrative.

With the Fed now cutting rates and the latest CME FedWatch tool now predicting the FOMC will cut by a quarter percentage point, down to 3.5% to 3.75% this week, it’s game on for CEFs.

The easy way they benefit is from the lower cost of borrowing. Obviously, it’s now cheaper for CEFs to borrow and invest in lower-dated assets. This has a dramatic effect on additional yield potential from the CEF. Distribution coverages rise, and we typically see an increase in managed distribution plans during declining rate environments. That’s good for income seekers.

A second, and behind-the-scenes, way CEFs win in a declining rate environment is NAV appreciation. As we said, CEFs tend to invest in longer-dated assets. As rates fall, prices for longer-dated bonds and securities tend to go up. Investors try to lock in yield. For CEFs, this creates a boost for their portfolio values and increases their net asset values, benefiting investors.

Ultimately, lower rates encourage investors to take on more risks. Cash and T-bills will quickly produce low returns; investors are forced to look at other alternatives for income and yield. That means cash is no longer king, but bonds and other higher-yielding securities are in.

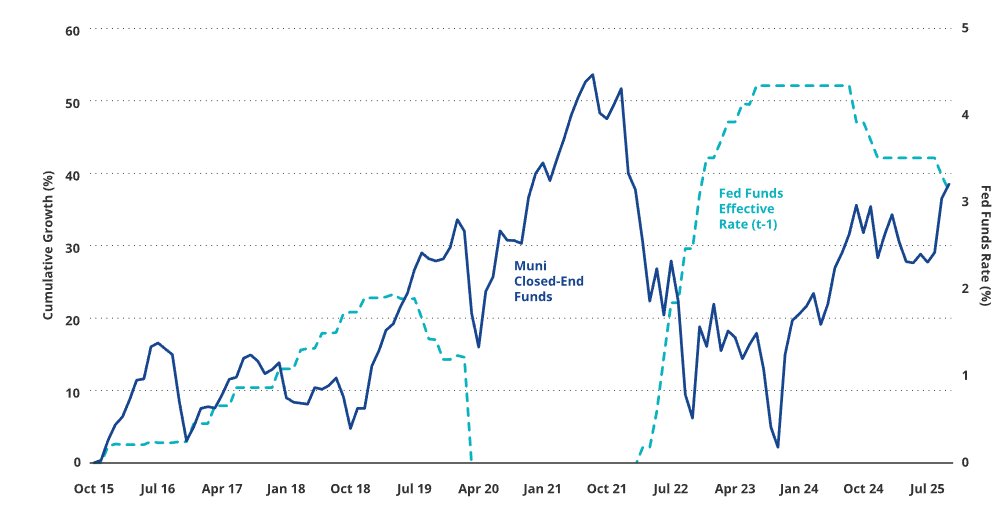

You can see this in action over time. Looking at this chart from VanEck of municipal bond CEFs, one of the largest categories of CEFs, you can see that when rates are declining, returns expand. The same is true for many other sectors of the CEF market, such as preferred securities, junk bonds, and senior loans.

Source: Van Eck

Data from BlackRock also supports this fact. Over the long term, leveraged municipal CEFs have outperformed unleveraged municipal CEFs in 13 of the last 20 years. Those 13 years? Periods of low and declining rates. 1

Adding CEFs in Anticipation of Rate Cuts

With the Fed now cutting rates, closed-end funds have a real chance to shine. The use of leverage and the enhancement of that leverage when rates are low is a key feature to boosting returns and income potential. For investors, the time to add the structure to their portfolio is now.

Keep in mind, positioning a portfolio for potential rate cuts involves more than simply choosing any high-yielding CEF. Investors should examine leverage ratios, what asset classes the fund owns, and the overall costs of that leverage before taking the plunge. But ultimately, lower interest rates are a boon for CEFs, their income, and total returns.

Top CEFs

These CEFs are sorted by their YTD total returns, which range from -2.3% to 15.8%. They have AUM between $100M and $1.65B and expenses between 0.85% and 4.3%. They are currently yielding between 6.1% and 13.1%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type |

|---|---|---|---|---|---|---|

| XAGIX | abrdn Global Infrastructure Income Fund | $610M | 15.83% | 12.66% | 2.04% | CEF |

| XBGRX | BlackRock Energy Resources Trust | $380M | 9.6% | 6.1% | 1.29% | CEF |

| XJQCX | Nuveen Credit Strategies Income Fund | $790M | 9.2% | 13.1% | 2.67% | CEF |

| XJFRX | Nuveen Floating Rate Income Fund | $1.22B | 8.7% | 12.8% | 3.4% | CEF |

| XBGTX | BlackRock Floating Rate Income Trust | $285M | 8.2% | 12.1% | 3.05% | CEF |

| XBDJX | BlackRock Enhanced Equity Dividend Trust | $1.65B | 7.3% | 9.1% | 0.86% | CEF |

| XJLSX | Nuveen Mortgage and Income Fund | $104M | 7% | 10.8% | 1.57% | CEF |

| XBDJX | BlackRock Enhanced Equity Dividend Trust | $1.5B | 6.68% | 8.55% | 0.85% | CEF |

| XBOEX | BlackRock Enhanced Global Dividend Trust | $627M | 6.59% | 8.8% | 1.07% | CEF |

| XJPCX | Nuveen Preferred Income Opportunities Fund | $783M | 6.5% | 9.3% | 2.68% | CEF |

| XIGAX | Voya Global Advantage & Premium Opportunity Fund | $154M | 6.07% | 10.16% | 1.1% | CEF |

| XBITX | BlackRock Multi-Sector Income Trust | $615M | 6% | 10.17% | 4.28% | CEF |

| XFFAX | First Trust Enhanced Equity Income Fund | $401M | 1.93% | 6.9% | 1.12% | CEF |

| XETVX | Eaton Vance Tax-Managed Buy-Write Opportunities Fund | $1.6B | -1.1% | 8.77% | 1.08% | CEF |

| XDIAX | Nuveen Dow 30 Dynamic Overwrite Fund | $517M | -2.34% | 8.47% | 0.92% | CEF |

Rate cuts can be a powerful catalyst for improved performance across the closed-end fund landscape. Thanks to their use of leverage, high distribution potential, and frequent discounts to NAV, CEFs are uniquely positioned to benefit when borrowing costs fall and market sentiment shifts. Historical data shows this as fact. For investors, adding CEFs to a portfolio could now be a great idea.

Bottom Line

For investors seeking to enhance income, reduce the drag from higher borrowing costs, and capture potential upside from a changing rate environment, CEFs offer a compelling and structurally advantaged opportunity.

1 BlackRock (December 2025). Spotlight on leverage in closed-end funds