For years, market pundits have pushed a narrative that the key to portfolio success, reduced trading costs, and better returns is to think big. That is, the most liquid and active ETFs are the way to go, and smaller ETFs should be ignored. Many investors have gravitated toward the largest ETF issuers and funds for their portfolio holdings, and the surge in active ETFs has pushed this narrative further, drawing investors toward the biggest funds.

However, this narrative may not hold water.

ETF liquidity is a complex network—one that doesn’t always favor funds with the highest average trading volumes. For many investors, including institutions, fund strategy rather than liquidity should be the chief concern.

The Misunderstood Metric of Liquidity

ETFs are a remarkable fund vehicle, offering the diversification benefits of mutual funds alongside daily tradability, which explains their rapid adoption. For many investors, ETFs have become the de facto way to build portfolios, yet evaluation often focuses on one major factor—in addition to cost, of course.

That would be average daily trading volume.

The logic seems straightforward: higher volume suggests tighter bid-ask spreads, deeper liquidity, and easier execution. Many investors therefore gravitate toward the largest and most actively traded ETFs, often avoiding smaller or lower-volume funds out of concern that they may be difficult or costly to trade.

This perception is reinforced by a common fear that low-volume ETFs carry wider bid-ask spreads, limited liquidity, and the potential for price dislocation during market stress—a fear largely rooted in equity market trading, where market demand dictates share pricing.

While heavily traded ETFs do tend to have tighter spreads, this view is incomplete. Focusing solely on average daily volume can lead investors to overlook how ETFs actually function, since the attributes of equity market trading do not carry over into the world of ETFs.

The Engine of ETF Liquidity

ETF liquidity is multilayered, and the trading volume visible on an exchange represents only a portion of the total available liquidity. As asset manager American Century notes, average daily volume reflects only what has been traded of an ETF, not what can be traded.

Thanks to the ETF structure, even funds with relatively low trading volume can offer substantial and reliable liquidity. Understanding this structure is key to making more informed investment decisions, and at its heart is the creation and redemption mechanism.

The creation and redemption mechanism is unique to ETFs and distinguishes the fund vehicle from traditional stocks and mutual funds in terms of trading and liquidity.

Unlike a stock, whose liquidity is limited to shares traded in the secondary market, an ETF’s supply is not fixed—it can expand or contract based on investor demand through institutional participants known as authorized participants (APs).

When demand for an ETF increases, APs can create new shares by delivering a basket of underlying securities to the ETF issuer in exchange for ETF shares, which they then sell in the market. When demand decreases, APs redeem ETF shares for the underlying securities. This process ties the ETF’s liquidity to that of its underlying holdings rather than to its own trading volume.

For example, an ETF tracking a broad equity index or a liquid bond market may trade infrequently on an exchange, yet if the underlying securities are highly liquid, APs can create or redeem shares as needed to ensure supply meets demand.

This means that even a low-volume ETF can support large trades without significantly moving its price, provided its underlying assets are liquid.

Beyond AP liquidity and on-screen liquidity, ETFs benefit from an additional layer of support through market makers—firms that continuously provide bid and ask quotes, facilitate trading, and help maintain orderly markets. Importantly, the liquidity they provide is not limited to what is visible on the exchange.

Market makers determine their quotes based on the value of an ETF’s underlying securities, as well as factors such as market conditions, volatility, and demand. Because they can hedge their positions using the underlying assets, they can provide liquidity even in ETFs with low trading volumes. What investors see on their screens—the quoted bid and ask sizes—represents only a snapshot of available liquidity. In reality, market makers are often willing to transact in much larger sizes than what is displayed, a concept sometimes referred to as implied liquidity. This ability to quote beyond visible liquidity creates market depth, allowing investors to execute trades that exceed the displayed size without significantly widening spreads.

The role of brokers and block trading cannot be ignored. Brokers and institutional trading desks play a crucial role in facilitating ETF transactions, particularly through block trading, which enables investors to transact in large sizes at negotiated prices often close to the ETF’s net asset value (NAV). This is especially important for institutional investors, though it is increasingly accessible to smaller investors through modern trading platforms. For example, brokers will often route smaller share trade amounts together for efficiency and better pricing. When an investor wants to execute a trade, a broker can source liquidity across multiple channels.

The key takeaway is that ETF liquidity extends far beyond what is immediately visible, and professional trading support can unlock additional layers of liquidity.

Smaller ETFs Can Equal Big Opportunities

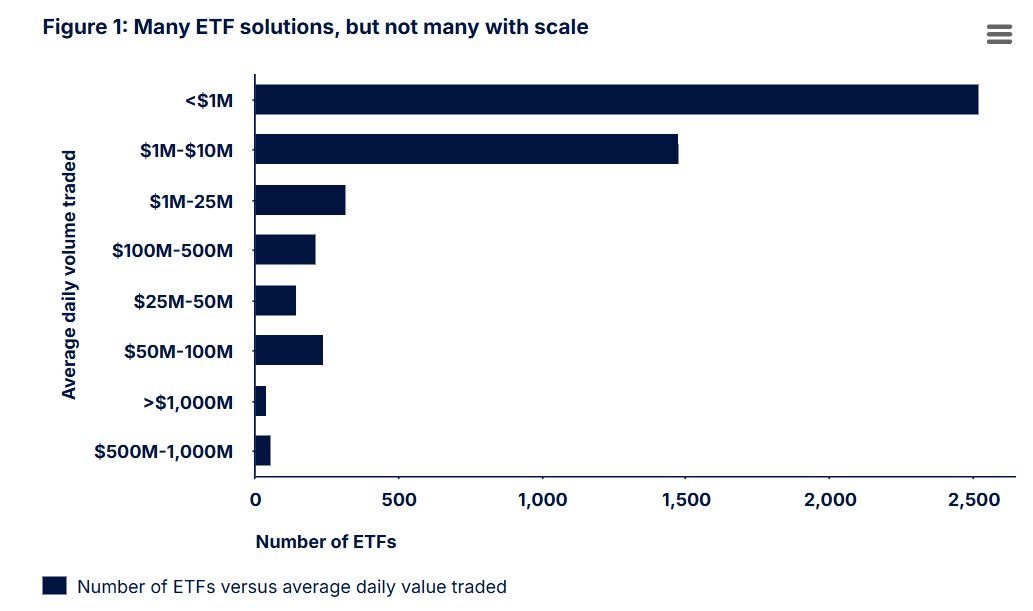

ETF liquidity extends far beyond what is immediately visible, and professional trading support can unlock additional layers of it. This is particularly important given the rise of active ETFs today. With numerous funds coming to market, many have limited average daily volume (ADV)—State Street reports that more than 86% of all U.S.-listed ETFs traded less than $25M per day on average during Q1 2026. 1

This chart from State Street shows this in practice.

Source: State Street

Instead of automatically excluding low-volume ETFs, investors should consider whether the fund’s underlying assets are liquid and whether it fits their portfolio needs. In many cases, the benefits of accessing a specific strategy or asset class may outweigh concerns about trading volume.

Popular Active ETFs

These active ETFs, sorted by 1-year total returns from 5.1% to 17.4%, have expense ratios of 0.17% to 0.36%, AUM from $11 billion to $42 billion, and yields from 0.8% to 11.2%.

| Ticker | Name | AUM | 1Y Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| JEPQ | J.P. Morgan Nasdaq Equity Premium Income ETF | $32 billion | 17.4% | 11.2% | 0.35% | ETF | Yes |

| DFAC | Dimensional U.S. Core Equity 2 ETF | $40 billion | 17.2% | 0.8% | 0.17% | ETF | Yes |

| DFUV | Dimensional U.S. Marketwide Value ETF | $12.6 billion | 17.1% | 1.5% | 0.21% | ETF | Yes |

| DFAT | Dimensional U.S. Targeted Value ETF | $11.8 billion | 10.4% | 1.6% | 0.28% | ETF | Yes |

| JEPI | JPMorgan Equity Premium Income ETF | $41.5 billion | 9.5% | 7.7% | 0.35% | ETF | Yes |

| AVUV | Avantis U.S. Small-Cap Value ETF | $19.4 billion | 9.2% | 1.4% | 0.25% | ETF | Yes |

| FBND | Fidelity Total Bond ETF | $22.9 billion | 7.8% | 4.4% | 0.36% | ETF | Yes |

| JPST | JPMorgan Ultra Short Income ETF | $35.3 billion | 5.4% | 4.2% | 0.18% | ETF | Yes |

| MINT | PIMCO Enhanced Short Maturity Active ETF | $14.5 billion | 5.1% | 4.4% | 0.36% | ETF | Yes |

While average daily volume is a useful metric, it represents only one part of the liquidity equation. The creation and redemption mechanism, the role of market makers, and the availability of broker-assisted trading all contribute to a deeper and more resilient liquidity structure.

In reality, many low-volume ETFs can offer ample liquidity, competitive pricing, and efficient execution—particularly when their underlying assets are liquid, and trades are executed thoughtfully.

Bottom Line

Average daily volume alone does not define an ETF’s true liquidity, and avoiding lower-volume funds can mean missing valuable opportunities. Thanks to the creation and redemption mechanism, active market makers, and access to deeper liquidity through brokers and block trading, many ETFs offer far more trading capacity than what appears on screen.

1 State Street (April 2026). Optimizing trade execution for ETFs of all levels of liquidity