Fixed-income investing is undergoing a quiet transformation. After years of ultra-low yields, bonds are once again offering compelling income opportunities. Investors can now earn meaningful yields across a wide range of sectors, from investment-grade corporates to securitized assets and beyond. However, as the opportunity set has expanded, so too has the realization that traditional benchmarks—particularly the Bloomberg U.S. Aggregate Bond Index, or “the Agg”—may no longer be enough.

In response, investors have increasingly turned to core-plus fixed-income strategies, with active ETFs as the vehicle of choice.

Not all core-plus strategies are created equal, and understanding what they are, why they have grown in popularity, and how to assess their strengths and risks is essential for building a modern fixed-income portfolio.

Why Core-Plus Has Gained Popularity

Since its creation in 1986, the Bloomberg U.S. Aggregate Bond Index (Agg) has grown to become the de facto benchmark for the bond sector, with billions of dollars now sitting in vehicles tied to the index.

However, despite its value, the Agg has drawbacks.

The Agg was designed to represent the U.S. investment-grade bond market, and as such, it is heavily weighted toward Treasuries and agency mortgage-backed securities. While these assets provide stability, they often offer relatively low yields. More importantly, the index is constrained by its rules—it reflects what is issued, not necessarily what is attractive. This limitation has become more visible as the Agg has shifted toward more Treasury debt as the U.S. bond pile has grown.

This has become increasingly problematic in today’s environment. Investors are no longer satisfied with tracking a benchmark that may underrepresent higher-yielding opportunities, and instead are seeking ways to capture more income while maintaining the core role of bonds: diversification and risk management.

Core-plus strategies address this gap by expanding the opportunity set.

A core bond portfolio typically focuses on high-quality, investment-grade securities with moderate duration, aiming to provide stability and income. Core-plus builds on this foundation by adding selective exposure to higher-yielding or more opportunistic sectors.

This “plus” component differentiates the strategy by allowing managers to go beyond the Agg and allocate across a broader range of fixed-income assets, including below-investment-grade bonds, emerging market debt, non-agency mortgages, asset-backed securities, and other segments that are underrepresented or excluded from traditional benchmarks.

Core-plus funds aim to generate total return through a combination of income and capital appreciation, with income as the dominant driver.

Picking a Core-Plus Active ETF

At their core—pun intended—core-plus bond funds are designed to replace and reduce the limitations of the Agg.

The active ETF structure has further accelerated adoption. Active bond ETFs provide daily liquidity, transparency, and often lower costs than traditional mutual funds, making core-plus strategies more accessible than ever. Adding the tax savings from ETFs’ creation-redemption mechanisms creates a recipe for success.

Perhaps the only challenge is figuring out which fund to purchase for a portfolio. Thanks to the active ETF boom, there are hundreds to choose from.

Evaluating core-plus fixed-income ETFs requires a different mindset than evaluating passive bond funds. Because these strategies are active and flexible, investors must look beyond simple metrics like yield or expense ratio, though a useful framework does exist.

The first step is to understand what the fund can actually invest in.

Core-plus strategies can vary widely in their mandates. Some may limit exposure to high-yield or emerging markets, while others may take more aggressive positions—certain strategies, for example, may allocate up to 35% of assets to high-yield or higher-risk bonds, which can significantly affect both yield and risk. Investors should examine how broad the opportunity set is and how it aligns with their risk tolerance, since a wider opportunity set can enhance returns but also requires strong risk management.

Secondly, it’s important to note that not all yield is created equal.

A key question is where the fund’s returns are coming from. Is the yield driven by high-quality credit exposure, or is it the result of significant credit or liquidity risk? Does the manager rely heavily on interest rate positioning, or is income the primary driver?

Core-plus strategies are typically designed to generate returns primarily from income, supplemented by capital appreciation—an important distinction, as income-driven returns tend to be more stable and predictable.

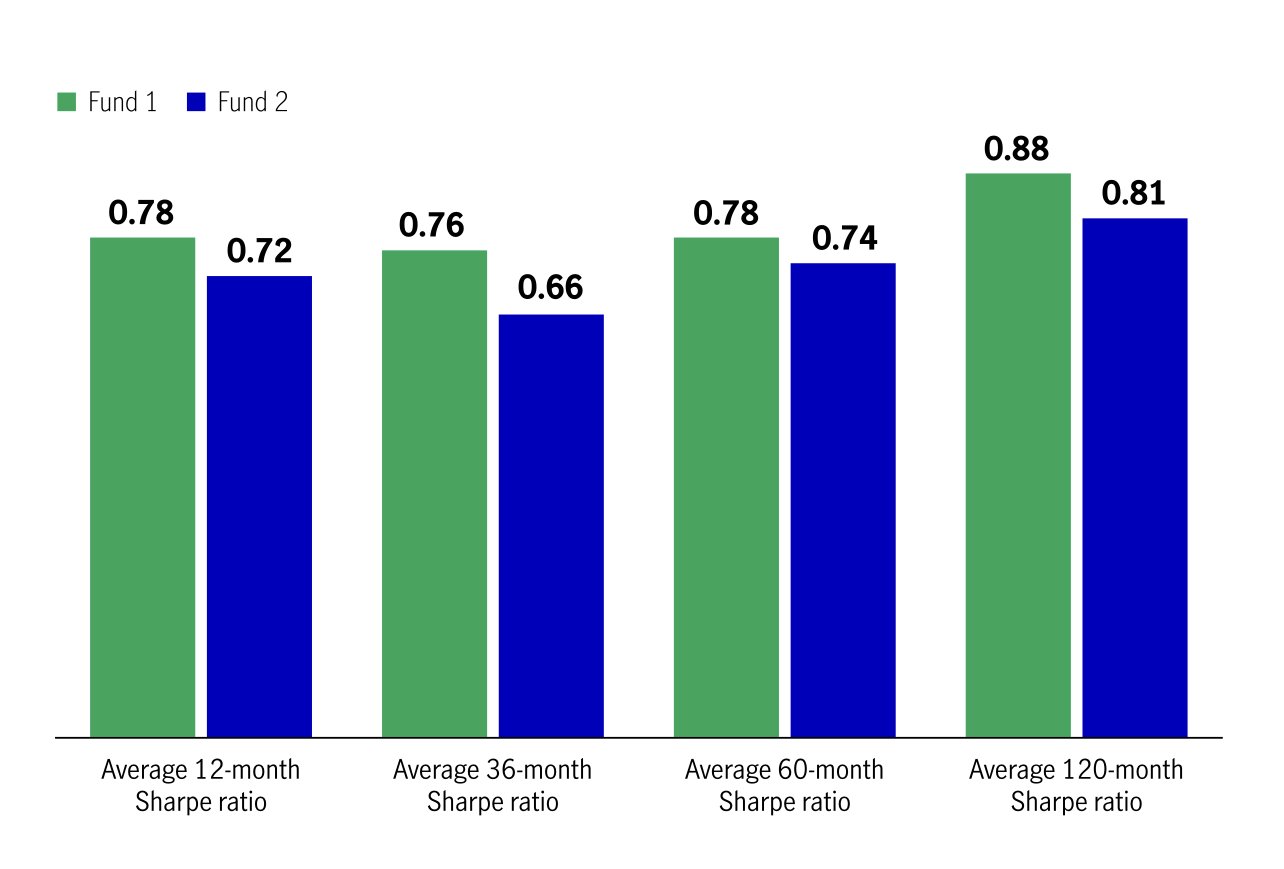

This plays out in risk management. Because these funds have flexibility, they also carry the potential for unintended risks. Investors should examine how the manager controls for credit risk, duration, liquidity, and sector concentration, as comparing Sharpe Ratios can reveal meaningful differences across core-plus funds.

This chart highlights how two different core-plus funds allocate differently to risk, despite belonging to the same fund category.

Source: Manulife

Investors should also evaluate the manager’s experience, research capabilities, and investment philosophy. Core-plus strategies often rely on deep credit analysis and sector expertise, making the quality of the investment team critical.

Finally, while active ETFs are generally more cost-effective than mutual funds, expenses still matter.

Investors should consider whether a fund’s fees are justified by its potential to add value. A higher expense ratio may be acceptable if the strategy consistently delivers better risk-adjusted returns, but lower expenses are generally preferable.

Together, these steps can help investors evaluate a core-plus fund and determine how it fits within a fixed-income portfolio.

Adding Core-Plus Into a Portfolio

For many investors, core-plus fixed-income ETFs can serve as a replacement for traditional core bond allocations.

Instead of allocating to a passive Agg-based ETF, investors can use a core-plus strategy as the foundation of their fixed-income portfolio, capturing higher yields and greater diversification without sacrificing the stabilizing role of bonds.

A smart approach may be to select more than one strategy across several managers to gain meaningful diversification benefits. Using the simple framework above, investors can make an informed choice for their core-plus allocation.

Ultimately, the goal is to build a portfolio that balances income, risk, and flexibility—something traditional benchmarks may struggle to achieve on their own.

Core-Plus ETFs

These ETFs were selected for their low-cost exposure to active bond management within the unconstrained, dynamic, and core-plus sectors. Sorted by YTD total return, they range from -1.2% to 2.8%, with expense ratios from 0.10% to 0.71%, assets from $63M to $18B, and current yields between 4.2% and 5.5%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| JCPB | JPMorgan Core Plus Bond ETF | $5.78B | 2.8% | 5.3% | 0.40% | ETF | Yes |

| BOND | PIMCO Active Bond ETF | $5.5B | 2.5% | 5.3% | 0.71% | ETF | Yes |

| VPLS | Vanguard Core Plus Bond ETF | $138M | 2.5% | 4.8% | 0.2% | ETF | Yes |

| TOTL | SPDR DoubleLine Total Return Tactical ETF | $3.5B | 2.3% | 5.1% | 0.55% | ETF | Yes |

| FBND | Fidelity Total Bond ETF | $18.1B | 2.2% | 5% | 0.36% | ETF | Yes |

| AVIG | Avantis Core Fixed-Income ETF | $1B | 2.2% | 5% | 0.15% | ETF | Yes |

| BINC | BlackRock Flexible Income ETF | $8.14B | 2.1% | 5.5% | 0.52% | ETF | Yes |

| FIXD | First Trust TCW Opportunistic Fixed-Income ETF | $4.32B | 2.1% | 4.3% | 0.65% | ETF | Yes |

| DBND | DoubleLine Opportunistic Bond ETF | $413M | 2% | 4.8% | 0.45% | ETF | Yes |

| DFCF | Dimensional Core Fixed-Income ETF | $243M | 2% | 4.6% | 0.19% | ETF | Yes |

| CGCP | Capital Group Core Plus Income ETF | $4.5B | 1.8% | 4.8% | 0.34% | ETF | Yes |

| VCRB | Vanguard Core Bond ETF | $63M | -1.2% | 4.2% | 0.10% | ETF | Yes |

The fixed-income landscape has evolved, and investors need to evolve with it. While the Agg remains a useful reference point, it no longer captures the full range of opportunities available in today’s bond market.

Core-plus fixed-income active ETFs offer a compelling alternative by expanding the opportunity set, focusing on income generation, and leveraging active management to provide a more modern approach to bond investing.

With greater flexibility comes greater responsibility. Evaluating these strategies requires a deeper understanding of their structure, risks, and sources of return.

Bottom Line

Core-plus active ETFs represent a modern evolution of fixed-income investing, offering broader opportunity sets, higher income potential, and more flexible risk management than traditional Agg-based strategies. However, their benefits depend heavily on how they are constructed and managed.