Bonds have historically been viewed as the “stable” part of a portfolio—a place for income, capital preservation, and diversification. However, the recent period has challenged that assumption. Price swings have increased, correlations have shifted, and volatility has become a more prominent feature of fixed-income markets.

For many investors, this shift has been uncomfortable.

Yet this new environment is not necessarily a negative. For investors willing to adapt their approach, fixed-income volatility can be a powerful source of opportunity and excess return.

A New Fixed-Income Landscape

The bond market today is defined by uncertainty—and that uncertainty is driving volatility.

Central banks are navigating a delicate balance between controlling inflation and supporting economic growth. Inflation, while lower than its peak, remains persistent in key areas, complicating policy decisions. Meanwhile, economic data has been mixed, with signs of both resilience and slowdown appearing simultaneously.

This has created a market where rate expectations are constantly shifting, with investors recalibrating their outlooks in real time as they react to new data, policy signals, and geopolitical developments.

The result is a fixed-income market far less predictable than it was during the previous decade—but with that unpredictability comes something important: dispersion and dislocation.

Volatility in fixed-income has increased significantly compared to the calm, low-rate environment of the 2010s.

Interest rate volatility has been particularly elevated. Moves in Treasury yields have been larger and more frequent, reflecting uncertainty around inflation and monetary policy, while yield curves have shifted dramatically—at times flattening, steepening, or inverting as markets reassess economic conditions.

This volatility is reflected in sharp moves in the MOVE Index (Merrill Lynch Option Volatility Estimate), which remains elevated relative to historic norms.

Credit markets have also experienced greater dispersion. Spreads between investment-grade, high-yield, securitized assets, and emerging market debt have fluctuated as investors reassess risk.

All of this has created rough waters for bond investors.

Volatility Creates Opportunity

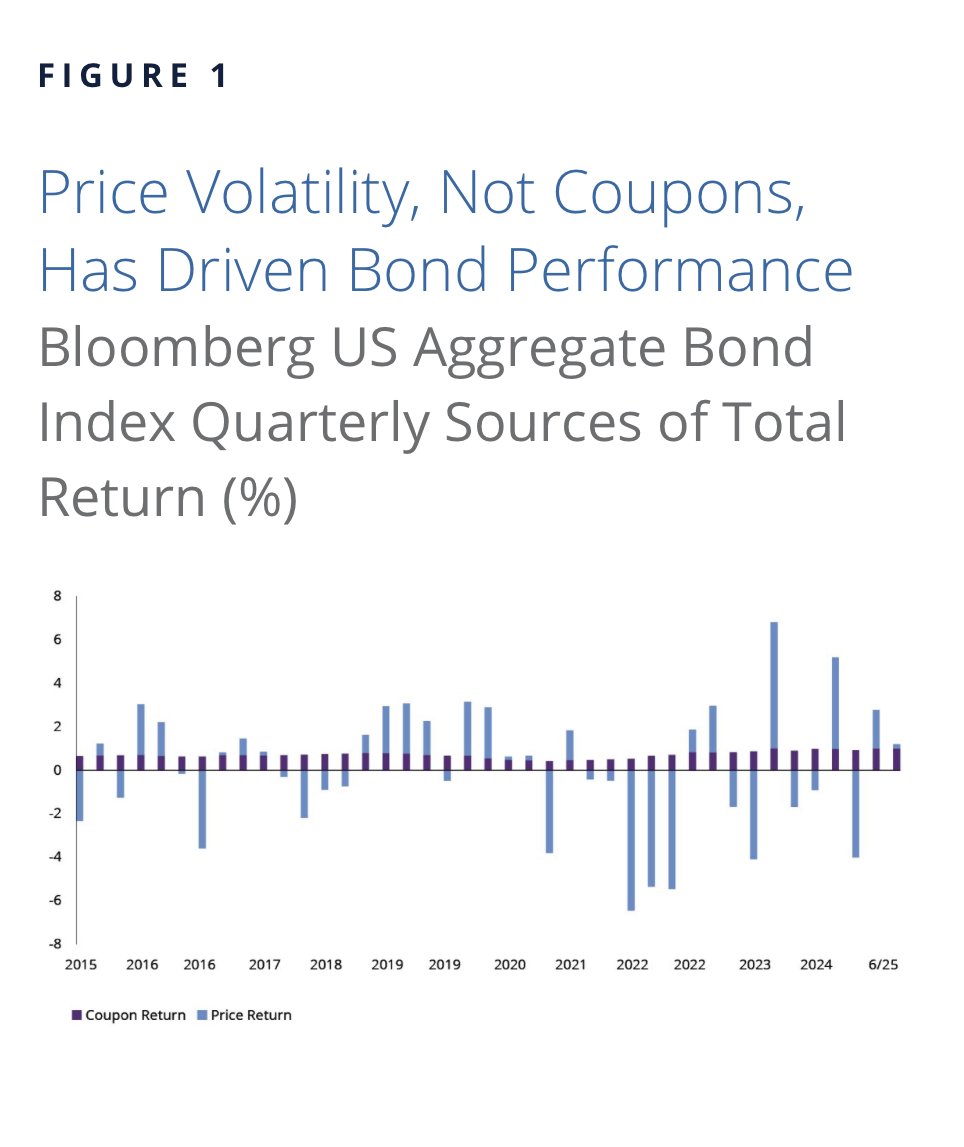

This volatility matters more to returns than coupon or yield. According to research by Hartford, price movements have accounted for about 61% of total fixed-income returns each quarter when examining the Bloomberg US Aggregate Bond Index (Agg) over the last decade. 1

This chart sums up their findings.

Source: Hartford

While volatility is often viewed as a risk, it can also be a source of return—especially in the fixed-income space.

In fixed-income markets, volatility leads to mispricings and dislocations. When markets react quickly to new information, prices can overshoot, creating opportunities to buy undervalued assets or sell overvalued ones.

For example, a sudden rise in interest rates may cause bond prices to fall sharply. However, if that move is driven by short-term sentiment rather than long-term fundamentals, it can create an opportunity to purchase high-quality bonds at attractive yields.

Similarly, widening credit spreads can reflect heightened risk aversion rather than actual deterioration in credit quality. Investors who can differentiate between the two can capture higher yields and potential price appreciation as spreads normalize.

This is one of the key ways volatility translates into returns. It creates entry points that would not exist in a more stable environment, allowing investors to capture higher yields and profit as prices recover and spreads tighten.

The focus now shifts to total returns rather than income alone.

Turning Volatility into Excess Returns

Capturing the benefits of volatility requires an active approach.

Passive strategies, by design, are tied to benchmarks and cannot take advantage of mispricings or adjust exposures in response to changing conditions, so they may miss opportunities created by volatility.

Active strategies are specifically designed to exploit these dynamics, giving active managers an edge by capitalizing on dislocations that volatility creates. Given the growing volatility in today’s bond market, that is one more reason to go active with your bonds. According to Hartford, this is exactly the environment that active management in fixed-income was made for.

The most effective way to harness fixed-income volatility is through active bond funds and ETFs.

These vehicles provide access to professional management, diversified exposure, and the ability to adjust portfolios dynamically. Active managers can navigate complex market conditions, identify opportunities, and manage risk in ways that individual investors find difficult to replicate.

Top Active Bond and Core-Plus ETFs

These ETFs were selected for their low-cost exposure to active bond management within the unconstrained, dynamic, and core-plus sectors. Sorted by YTD total return, they range from -1.2% to 2.8%, with expense ratios from 0.10% to 0.71%, assets from $63M to $18B, and current yields between 4.2% and 5.5%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| JCPB | JPMorgan Core Plus Bond ETF | $5.78B | 2.8% | 5.3% | 0.40% | ETF | Yes |

| BOND | PIMCO Active Bond ETF | $5.5B | 2.5% | 5.3% | 0.71% | ETF | Yes |

| VPLS | Vanguard Core Plus Bond ETF | $138M | 2.5% | 4.8% | 0.2% | ETF | Yes |

| TOTL | SPDR DoubleLine Total Return Tactical ETF | $3.5B | 2.3% | 5.1% | 0.55% | ETF | Yes |

| FBND | Fidelity Total Bond ETF | $18.1B | 2.2% | 5% | 0.36% | ETF | Yes |

| AVIG | Avantis Core Fixed-Income ETF | $1B | 2.2% | 5% | 0.15% | ETF | Yes |

| BINC | BlackRock Flexible Income ETF | $8.14B | 2.1% | 5.5% | 0.52% | ETF | Yes |

| FIXD | First Trust TCW Opportunistic Fixed-Income ETF | $4.32B | 2.1% | 4.3% | 0.65% | ETF | Yes |

| DBND | DoubleLine Opportunistic Bond ETF | $413M | 2% | 4.8% | 0.45% | ETF | Yes |

| DFCF | Dimensional Core Fixed-Income ETF | $243M | 2% | 4.6% | 0.19% | ETF | Yes |

| CGCP | Capital Group Core Plus Income ETF | $4.5B | 1.8% | 4.8% | 0.34% | ETF | Yes |

| VCRB | Vanguard Core Bond ETF | $63M | -1.2% | 4.2% | 0.10% | ETF | Yes |

The fixed-income market has changed, and that change has brought increased volatility. While this may seem unsettling, it also represents one of the most significant opportunities in years.

Volatility creates dislocations, raises yields, and increases dispersion—all of which can be harnessed to generate excess returns. For investors willing to embrace an active approach, this environment offers the potential for both income and capital appreciation.

Volatility is not something to be feared. It is something to be understood and used.

Bottom Line

Fixed-income volatility is no longer just a risk—it’s an opportunity. Higher yields, wider spreads, and market dislocations are creating better entry points, allowing active investors to capture income and potential price gains through smart positioning and security selection.

1 Hartford (January 2026). How Volatility Is Reshaping Bond Returns