Arguably, one of the biggest battles in portfolio construction is whether active or passive management styles work best. Passive strategies have long dominated for numerous reasons, with active management emerging as an exception in certain pockets and sectors. The trend of losing this fight is well known for large-cap stocks.

However, things may be looking up for active large-cap strategies.

The efficient market hypothesis and the zero-sum perspective on active management of large-cap stocks now appear to be outdated concepts. New research shows that active stock pickers may finally have the last laugh, and active ETFs are helping them win.

Longterm Underperformance

It’s no secret that indexing has revolutionized portfolio construction. Ever since Vanguard founder Jack Bogle launched the first index fund in 1976, passive management has enjoyed a significant swell. By offering a simple and transparent way to invest in a broad market segment by tracking an index like the S&P 500, passive management has become the go-to for many investors to build their core portfolios. More importantly, passive investors enjoyed long-term outperformance when compared to their active rivals.

Part of that has to do with fees, trading costs, taxes, and the overall difficulty of timing the market in an effective manner. Active management has been successful in sections of the market or asset classes that provide market inefficiency, such as small-caps, junk bonds, and emerging markets.

That’s just the issue: market efficiency.

The idea is that when it comes to large-cap, U.S. stocks, investors can digest all the information and potential scenarios with ease. How many news and stock reports come out about Apple Inc every day? NVIDIA Corp has 59 different analysts covering it.

Because of this, there is an idea that active investing in very effective markets has to be a so-called zero-sum game. Here, for any active investor to outperform, another has to underperform. With that, it becomes hard to outperform; therefore, it’s easier to be passive and own them all.

Enhanced Indexing and the Rise of “Stock Pickers”

However, new research from investment manager Schroders highlights that the so-called zero-sum game may no longer be the correct way to think. Active ETFs are contributing to a shift where active management is beginning to outperform passive strategies within the large-cap stock space.

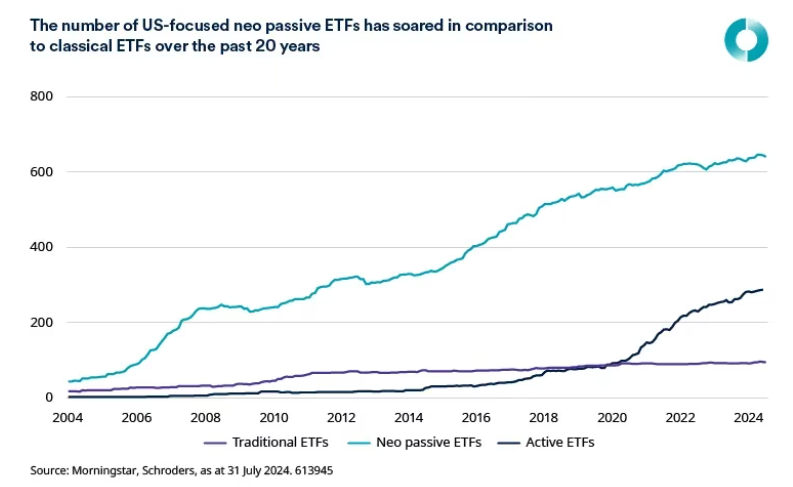

This chart from the asset manager shows an interesting trend.

Source: Schroders

What you are looking at is a chart of the number of traditional ETFs, active ETFs, and what Schroder’s calls neo-passive ETFs. Here in the U.S., we refer to them as enhanced indexing or systematic strategies. These funds take an index and apply small active adjustments to the benchmark. This can include applying value screens, looking for strong balance sheets, or scoring momentum and dividend yields. Managers use these systematic elements to purchase stocks or bonds to tweak an index. According to Schroder’s, there are now over six times as many of these [systematic funds] as traditional ETFs, and inflows have been 50% higher than traditional ETFs since 2018. 1

The premise that it must be a “this or that” scenario—the zero-sum game argument—is weakened by the fact that a large volume and value of investments are not strictly allocated based on broad market weights. For example, examining systematic ETFs, Schroders found that active positioning is a vast ocean. Looking at Apple alone, active ETFs can be as much as +2% overweight or as much as -7% underweight the stock. But it’s still there; it’s not an all-or-nothing situation.

And in that, investors can be more optimistic about the future of active management than in the past. Enhanced indexing allows active management to perform well and remove the so-called zero-sum argument from the equation, creating efficiencies and moving towards returns.

Now, Schriders argues that not every active ETF will beat a passive ETF. But it is mathematically possible, and investors shouldn’t ignore active indexing when they build their portfolios.

Betting on Active ETFs and Enhanced Returns

With Schroders’ report in mind, investors can now rest assured that active ETFs can outperform. Math isn’t holding them back. Enhanced indexing and systematic strategies work and can deliver on promises. As more investors and funds enter the arena, investors should look forward to the slight tweaks that can enhance their ability to perform.

Popular Active ETFs

These ETFs are sorted by their YTD total returns, which range from 3.1% to 18.4%. They have expense ratios between 0.17% and 0.70% and assets under management between $500 million and $42 billion. They are currently yielding between 0% and 9.7%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| CGGR | Capital Group Growth ETF | $16.7B | 18.4% | 0.4% | 0.39% | ETF | Yes |

| FBCG | Fidelity Blue Chip Growth ETF | $4.9B | 15.5% | 0.5% | 0.60% | ETF | Yes |

| TCHP | T. Rowe Price Blue Chip Growth ETF | $1.6B | 15.1% | 0% | 0.57% | ETF | Yes |

| JEPQ | J.P. Morgan Nasdaq Equity Premium Income ETF | $30.9B | 11.4% | 9.7% | 0.35% | ETF | Yes |

| DFAC | Dimensional U.S. Core Equity 2 ETF | $38.4B | 11.3% | 0.8% | 0.17% | ETF | Yes |

| DFUV | Dimensional US Marketwide Value ETF | $12.3B | 9.2% | 1.5% | 0.21% | ETF | Yes |

| FBND | Fidelity Total Bond ETF | $21.1B | 7.2% | 4.9% | 0.36% | ETF | Yes |

| JEPI | JPMorgan Equity Premium Income ETF | $41.3B | 5.4% | 7.4% | 0.35% | ETF | Yes |

| HYBL | SPDR Blackstone High Income ETF | $511M | 5.6% | 8.2% | 0.70% | ETF | Yes |

| JPST | JPMorgan Ultra Short Income ETF | $34.1B | 4.4% | 5.2% | 0.18% | ETF | Yes |

| AVUV | Avantis U.S. Small-Cap Value ETF | $18.6B | 4.1% | 1.4% | 0.25% | ETF | Yes |

| MINT | PIMCO Enhanced Short Maturity Active ETF | $14B | 4.1% | 5.3% | 0.35% | ETF | Yes |

| DFAT | Dimensional U.S. Targeted Value ETF | $11.6B | 3.1% | 0.8% | 0.28% | ETF | Yes |

All in all, the so-called zero-sum argument between passive and active funds is now blurred. With the rise of enhanced indexing and neo-passive vehicles, active ETFs are leading the way in helping drive outperformance in active management. With math now on their side, investors should consider active ETFs for their portfolios.

Bottom Line

The battle between active and passive ETFs has been a long and arduous fight. However, one of the main reasons active management has lost out on the zero-sum argument may be a thing of the past. The rise of enhanced indexing has made it all possible.

1 Schroders (2025-10). Think the US large cap market is too efficient for active managers to outperform? Time to think again