There’s no doubt that investment capital has shifted from active to passive management over the past couple of decades. With higher fees and more turnover, many active fund managers have found it challenging to outperform benchmark indices. Exchange-traded funds (ETFs) have also made it easier for investors to invest in passive market indexes.

While most active managers cannot consistently outperform the S&P 500, there are corners of the market where active fund managers regularly outperform indexes – such as fixed income. There are some instances where they can better find opportunities or reduce risks, but in other cases, simple market mechanics make passive indexing a challenge.

Let’s take a look at why active managers continue to outperform passive indexes in fixed income and some important factors that investors should keep in mind.

Be sure to explore our Fixed Income Channel to learn more about income generating strategies.

Active Managers Dominate Fixed Income

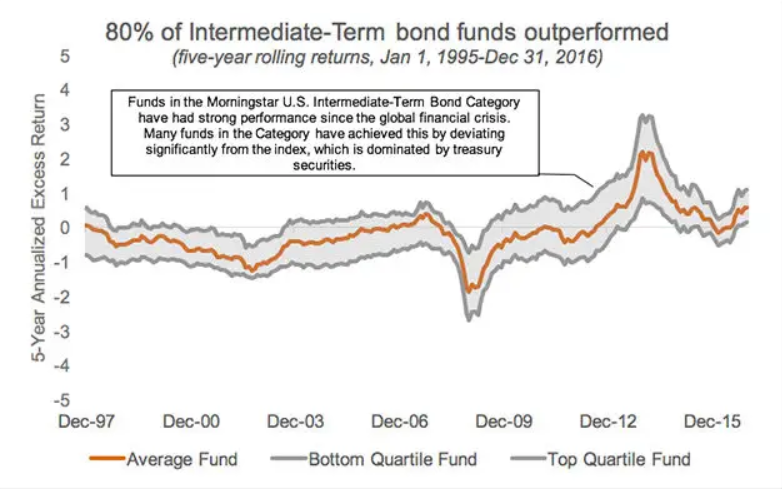

Active fixed-income strategies may offer more benefits to investors than passive index strategies. While less than 20% of active large-cap funds outperform passive benchmarks, nearly 80% of intermediate-term bond funds outperform their passive counterparts, according to Russell Investments, which flips a common investment truism on its head.

Active Outperforms Passive – Source: Russell Investments

There are a couple of structural reasons for the outperformance:

- Credit Risk: Fixed-income securities are weighted by the market value of their outstanding debt, which means that the most indebted issuers make up more of the index total. Active managers can use rigorous credit analysis to identify the most compelling opportunities rather than blindly buying high-risk bond issues.

- Interest Rate Risk: Duration has increased over time due to the higher weight of Treasuries, along with increased issuance of long-term corporate debt. While index fund durations have risen – thereby, increasing interest rate risk, active managers have greater flexibility in reducing interest rate risk with shorter durations.

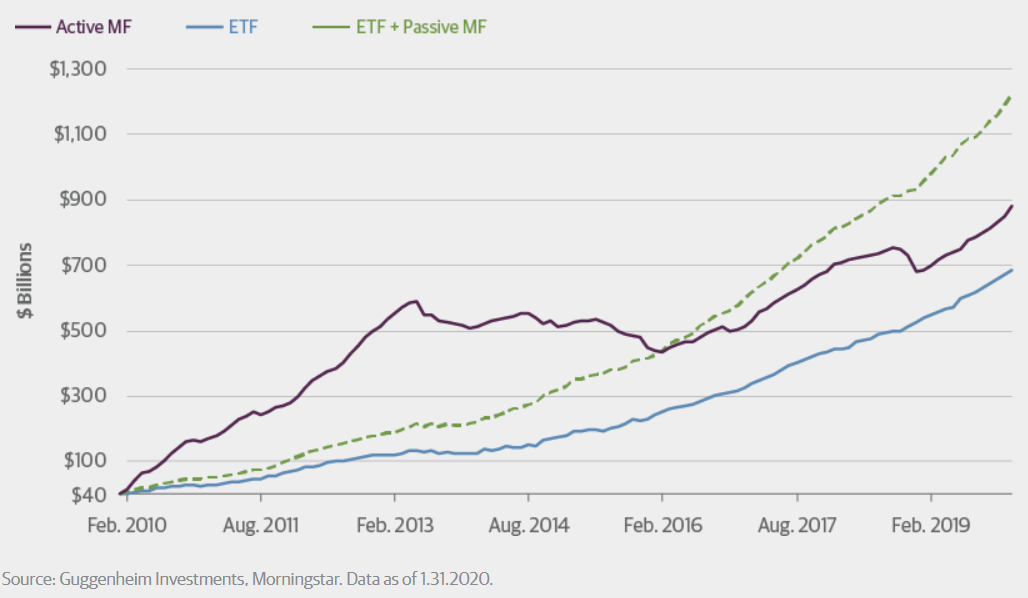

Despite these benefits, passive income investing continues to grow at a faster rate than active income investing. Many passive investors have transitioned into safe-haven fixed-income securities amid the COVID-19 pandemic while the outperformance of equities has led to some rebalancing into fixed income – often via passively managed funds.

Inflows into Passively Managed Fixed Income Funds – Source: Guggenheim

Passively managed fixed-income funds may be experiencing the majority of capital inflows, but actively managed fixed income still has the most assets under management.

Another point to note is that the trend from active to passive management has been much more pronounced for equities than fixed income. In fact, passive strategies represent just a third of total fixed-income mutual fund assets.

Our Best Dividend Stocks List has 20 of the highest-rated stocks by our proprietary Dividend.com Rating system. Go Premium to find out the entire list.

Impact on the Market & Investors

Many investors have embraced passively managed index funds as a way to build a low-cost portfolio. While passive funds make sense with large-cap equities, investors should think twice before embracing the same passive strategy across the board – especially given the growing body of evidence that actively managed fixed-income funds have outperformed passive funds.

There are also several instances where passively managed fixed-income funds could affect pricing and liquidity across the larger market. While these effects are obvious in large-cap equities (e.g., a drop in Apple’s price meaningfully impacts the entire S&P 500 Index), the effects on fixed-income investments are a little less certain and difficult to ascertain.

The most significant impacts include:

- Passive Funds Buying: Inflows into passively managed fixed-income funds affect the biggest borrowers in the index. In some cases, this can translate into a concentrated exposure to specific bonds and increased interest rate risk through higher duration.

- Passive Funds Selling: Outflows from passively managed index funds can impact liquidity and pricing in certain asset classes. For instance, a corporate bond downgrade could trigger investment-grade funds to automatically sell the bond at any price.

Some regulators worry that passive fixed-income investing could lead to persistent price distortions of individual bonds from fundamentals and excessive co-movements in the return of individual bonds. While some of these concerns also exist in equities, the risks could be amplified in the bond market due to its structural differences.

Use the Dividend Screener to find high-quality dividend stocks.

The Bottom Line

The transition from active to passive investments has been picking up steam for decades, but that doesn’t mean that it’s always the best option for investors. In the fixed-income space, there’s a growing body of evidence that active managers can outperform passive indexes by reducing credit and interest rate risk while ensuring proper diversification.

Keep track of the latest news in our News section, where we regularly publish the latest around dividend investing.